The brakes are being applied to capital expenditures given an increase in the cost of capital over the past year. CapEx plans within the S&P 1500 are poised to drop in 2023 to +7% from last year’s +21% increase.

Citi Research analysts are of the long-standing view that S&P 500 earnings would prove resilient relative to historical recession compares. This hasn’t changed. But they say they are increasingly concerned that current earnings resilience will translate into a longer period of subpar earnings growth.

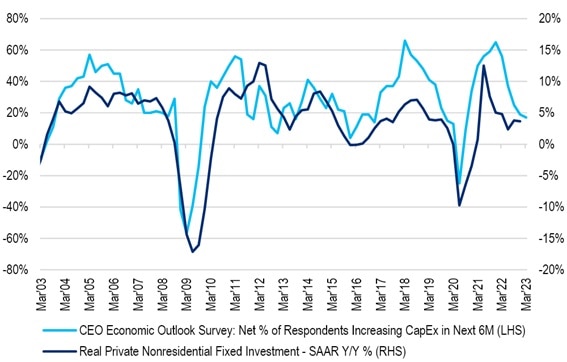

CEO Economic Outlook Survey: Capital Spending Plans

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Citi Research, Haver Analytics

CapEx grew 21% in 2022. S&P 1500 constituents spent, in aggregate, just over $1 trillion. Spending reflected 2021’s broader equity market strength as well as some catch up from the pandemic period. From here, CapEx growth is expected to be more muted, +7% in 2023, along with a flattish (+2%) early look at 2024.

Several months ago, the team highlighted a growing concern that rising cost of capital could be incrementally negative for CapEx, albeit positive for cash flow (see US Equity Strategy: New Era for the Cost of Capital: Equity Market Implications, dated 20 January 2023). The tradeoff in this is stronger short-term financial metrics but perhaps at the expense of long-term growth.

Relatedly, one entity’s CapEx is another entity’s source of revenues. However, that is tricky to quantify. But to the degree that last year’s CapEx surge supported earnings resilience, decelerating CapEx also presents an incremental demand hurdle for many companies/suppliers.

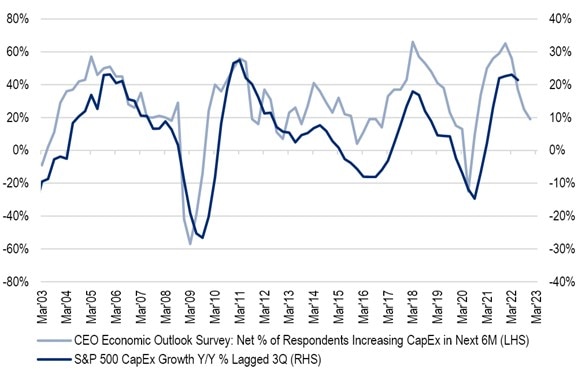

S&P 500 CapEx vs CEO Economic Outlook Survey

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Citi Research, Haver Analytics, Bloomberg

Another takeaway, the authors note, is an acknowledgement of the CapEx concentration within the S&P indices and, related, to the degree that reflects the influence of the mega-cap growth cohort.

The sector and industry group spending patterns can be informative. A sharp increase in Energy sector spend this year provides a tailwind to broader Industrials activity. Similarly, Utilities are a big driver of aggregate CapEx spending, with a +10% increase planned for 2023. On the flipside, Tech spending is projected to decline this year, as Semis CapEx tapers off from last year’s surge.

The broader S&P CapEx picture needs some context. The top 20 CapEx spenders will contribute 34% of the aggregate.

Generally, last year’s CapEx spending surge aligns with the post-Covid spending rebound. In turn, a decelerating pace of CapEx should sync with a gradual improvement in broader inflation metrics.

It does seem though that C-suites are incrementally less enthusiastic about CapEx plans.

In conclusion, S&P 1500 consensus data suggests that CapEx is set to decelerate in 2023 on the heels of a 2022 post-pandemic surge. Sector differences play into this, as do concentration effects.

There is a circular argument at work where EBITDA trends lead CapEx, but lower CapEx can also be a fundamental headwind to the beneficiaries of that spend. Lending standards, and credit conditions more broadly, suggest incremental pressure on spending.

For more information on this subject, please see the report dated 31 March 2023: US Equity Strategy - CapEx Complications

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.