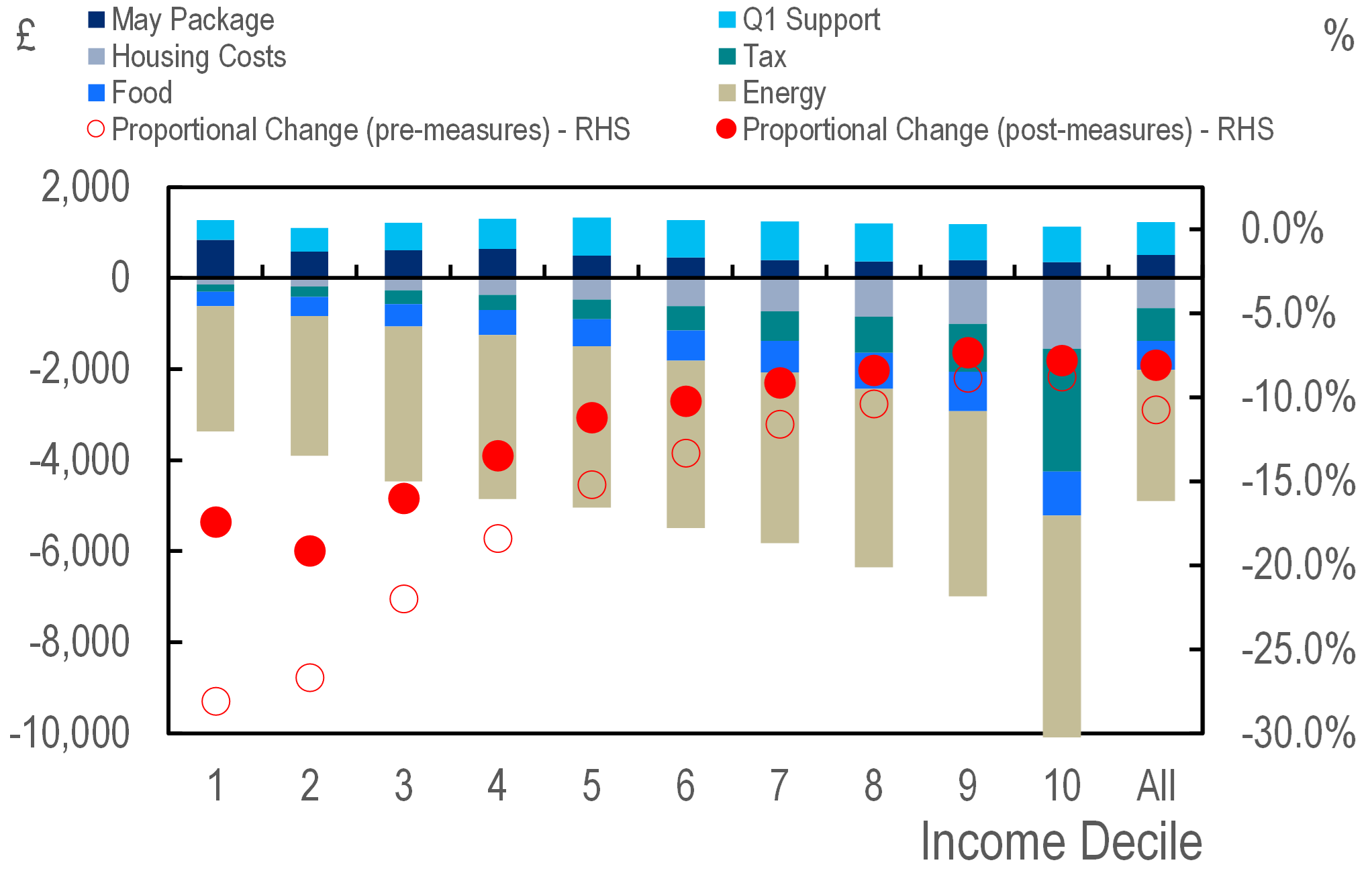

Ofgem: how bad can it get? — Ofgem recently raised the energy price cap from October to £3,549 a year. Citi expects further increases to £4,567 in January and then £5,816 in April. The risks here remain skewed to the upside.

Will policy offset the impact? — With rising affordability concerns, the question is what policy responses will prove most palatable and effective.

Policymakers are essentially juggling three types of intervention:

1) changes in indirect taxation

2) direct (and more widespread) measures to cap increases in energy bills

3) ex-post (often targeted) cash transfers.

The fundamental trilemma is between finding measures that are both affordable and provide the right demand incentives, but also minimize the risk of more persistent inflation. While the precise final balance is tricky, the focus on measures such as sweeping VAT cuts could strike a suboptimal balance. Citi analysts think the focus should remain on targeted cash support, and a cap on further increases in household bills – if at higher than current prices.

Any government response is likely to involve substantially more fiscal firepower (around £40bn, Citi analysts say). Offsetting the energy increase in full would cost around £30bn for the coming six months (1.4% of GDP). The issue for inflation is whatever fiscal space is deployed is likely to be squeezed between weaker medium-term forecasts and the desire to cut taxation. This means disinflationary measures are likely somewhat further down the pecking order.

How will the Bank react? — Even with the UK economy softening, recent data has re-affirmed the continued risk of pass-through from headline inflation into wage and domestic price setting could accelerate. Citi analysts expect the MPC will conclude the risks surrounding more persistent inflation have intensified, meaning a rising risk of rates heading into restrictive territory.

|

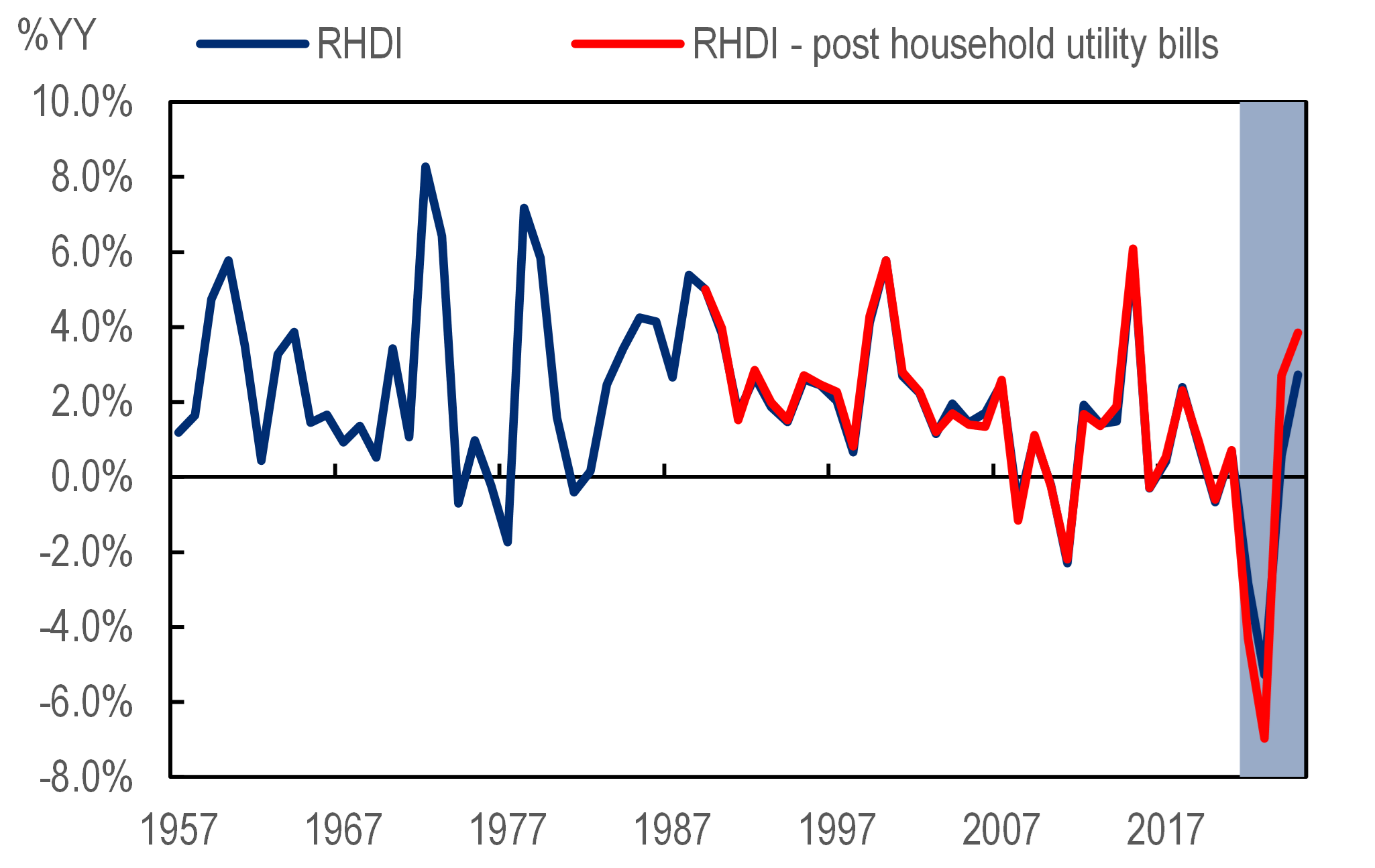

UK – RHDI (%YY), 1955-2025 |

|

|

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, ONS |

Source: Citi Research, ONS |

Understanding the scale of the issue — The recent rally in European gas prices means the UK is now in the midst of one of the most severe terms of trade shocks in its modern economic history. With UK gas prices having increased nearly tenfold since the Q3-2021, the share of nominal spending on gas in the UK is set to increase from 0.5% of GDP in 2019 to 7.6% in 2022. Even with a demand response, the share of spending could increase to a little over 6%. For electricity, the equivalent increase is a little less extreme – increasing from 2.2% to 7.3% absent a demand response. But even so recent price increases still leave the non-energy component of the UK economy nearly 10% worse off, say Citi economists.

For more information on this subject, please see the following notes UK Economics - Monthly Inflation Profiles and UK Economics - What is policy to do?

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.