Moderating wage and price inflation, an unemployment rate that remains surprisingly low and an economic trajectory that feels broadly in line with a soft landing. Can the current state of play in the U.S. continue?

A recent Citi Research report look at five episodes of wage disinflation since 1965 in search of clues.

Global Chief Economist Nathan Sheets and team continue to think that a period of rising unemployment, with a corresponding economic downturn, will be needed to loosen up a tight U.S. labor market and associated wage and services inflation. But they admit that the economy’s resilience and increasing signs of disinflation make that a tough call.

To help make that call, the team looks at the recent evolution of U.S. wage data, considering how much further wage growth will need to fall to bring inflation into line with the Fed’s expectations. And what would such an adjustment likely mean for the unemployment rate? In tackling these questions, Sheets and his team look at five episodes of significant U.S. wage disinflation since 1965.

Their findings: All five episodes were associated with periods of recession. To get meaningful traction bringing down wages, a broader slowing of the economy has been needed, with a marked rise in the unemployment rate. To be more specific, in these episodes two percentage points of wage deceleration looks to be associated with a two to three percentage-point rise in unemployment.

Those findings lead the authors to conclude that despite encouraging signs in recent data, “there are few antecedents in the U.S. experience for anything approximating a soft landing.” If there is to be a soft landing, the case has to be made for why this time will be different.

Looking at wage data

As a first step, Sheets and team ask: What pace of wage growth is likely to make Fed Chair Powell and his colleagues comfortable? The Fed is looking for wages to rise at a pace consistent with its inflation target, which suggests to the authors underlying wage growth of roughly 3% to 3.5%—the sum of the 2% inflation target plus their estimate of trend labor productivity growth, which looks to be around 1% to 1.5%. The intuition, they write, is that rising productivity increases firms’ margins and allows them to pay higher wages without additional price hikes, essentially financing higher wages with higher productivity.

To evaluate wage performance, the authors looked at two principal measures of wage growth: average hourly earnings (AHE) and the employment cost index (ECI). The two generally move together, and both indicate wages are now up roughly 4% to 4.5% from a year ago. Moreover, both of those series indicate wage growth has moderated: The 12-month change in AHE peaked at 5.9% in March 2022, while ECI peaked at 5.1% in 2022’s second quarter.

Labor Productivity Growth

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

*Note: Shading represents recessions.

Source: Citi Research, BLS, NBER, Haver Analytics

Wage Growth

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Citi Research, BLS, Haver Analytics

By the authors’ reckoning, wage growth is still running 1 to 1.5 percentage points above the Fed’s desired range. From the Fed’s perspective, a key risk is that this still-rapid wage growth gets embedded in workers’ expectations for future wage gains and ultimately in prices. Once that occurs, it becomes difficult for central banks to regain control of inflation.

This raises a central question for U.S. economic performance: How much does the unemployment rate need to rise to slow wage growth from its recent 4% to 4.5% readings to the “safety zone” of 3% to 3.5% likely consistent with the Fed’s 2% inflation target?

Five episodes of wage disinflation

With that central question on the table, Sheets and his team look to answer two queries:

1. In previous episodes of rapid wage inflation, how much has the unemployment rate risen as conditions adjust?

2. Have those episodes typically been associated with recessionary conditions?

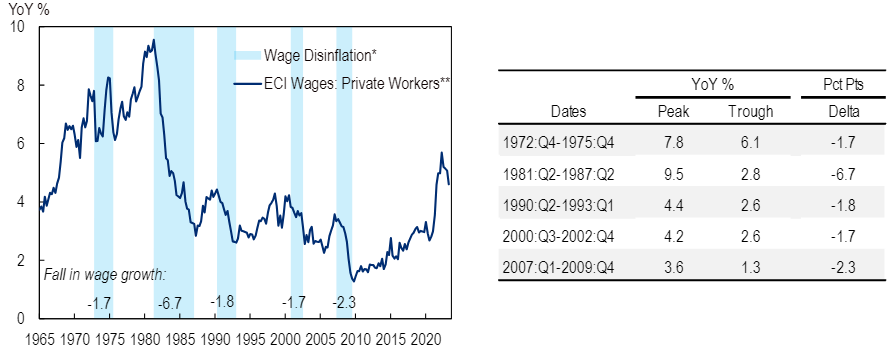

The authors address those questions by studying five significant episodes of wage disinflation, where a drop in wage growth of more than 1.5 percentage points was seen for at least two years. They are the first oil shock (1972-1975), the Volcker disinflation (1981-1987), the early 1990s, the dot-com crash (2000-2002), and the Global Financial Crisis (2007-2009).

ECI Wage Disinflation Cycles

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

*Shading denotes periods when wage growth fell at least 1.5 pct pts over two years or longer. **ECI is backcast from 1975:Q3 using its relationship with AHE of production & non-supervisory employees.

Source: Citi Research, BLS, Haver Analytics

The authors note that wage growth in the current cycle peaked at 5.7% in 2022’s second quarter and had fallen to 4.6% a year later. That means the peak-to-trough wage-growth adjustment needed to return to the Fed’s safety zone looks to be around 2.5 percentage points, with some 1.5 percentage points still remaining. The authors also note that in four of the five historical episodes they looked at, the wage disinflation that occurred was between 1.5 and 2.5 percentage points, broadly similar to the peak-to-trough adjustment needed in this cycle. (The Volcker disinflation was the outlier.)

In the last four episodes, wage growth fell to roughly 2%, near the Fed’s inflation objective. That’s below the authors’ estimate of the sustainable “run rate” for wages, which suggests that just as wages tend to cyclically overshoot when labor markets are tightening, they tend to undershoot during subsequent periods of wage disinflation. Which leads the authors to what they call a stark implication: If wage growth undershoots its sustainable run rate and falls to 2%, as happened in the four previous episodes, perhaps we need to consider the possibility of a larger wage disinflation than the 1 to 1.5 percentage-point estimate.

Finally, the authors note that all five wage-disinflation episodes were associated with recessions, leaving no example of significant wage disinflation of the magnitude currently required without a recession. That suggests that to get meaningful traction bringing down wages, a broader economic slowdown is necessary.

Unemployment implications

As wage growth slowed during the five episodes studied, how much did the unemployment rate rise? Broadly speaking, these periods saw rises in the unemployment rate ranging from 2.25 percentage points in the early 1990s and the dot-com crash to nearly 5.5 percentage points through the Global Financial Crisis.

Wage growth, the authors note, is typically still rising at a solid pace as it approaches its peak. It then tends to fall off sharply, by roughly 2 percentage points, over the following six quarters or so, with all five cycles seeing an appreciable rise in the unemployment rate following the wage-growth peak.

The team’s work leads to an interesting insight into a “typical” U.S. business cycle: Wage growth flattens out as it moves toward its peak, then falls off sharply—by 2.1 percentage points—over the following quarters. The unemployment rate, meanwhile, moves sideways and then inflects upward, rising 2.7 percentage points on average. The relationship between the two looks to be roughly one for one.

The authors’ conclusion is that the behavior of wage growth through the current cycle has broadly resembled previous ones. But the unemployment rate has diverged, remaining low with the labor market staying tight. A similar lag was seen in the 1972 cycle, a comparison that gives the authors pause as it was the Fed’s least durable disinflation effort.

Intrigued and beguiled

Reviewing the evidence from their investigation, Sheets and team note the association shown between wage disinflation cycles, increases in the unemployment rate and periods of recession. But they admit to being intrigued (and perhaps beguiled) by the pattern of recent U.S. data, with the unemployment rate staying low amid declines in wage growth and inflation.

Can this favorable performance persist? The authors call a soft-landing scenario “certainly possible,” but caution that their work clearly indicates it would be unique relative to the experience of the past six decades. So is there a case to be made that “this time is different?”

The authors note one striking feature of the current cycle: Inflation expectations have remained well anchored, which likely reflects a combination of credibility accumulated by the Fed and the effect of a decade of soft inflation before the pandemic.

Those expectations give the Fed more room to maneuver, the authors argue: It can remain patient and see how the economy performs, allowing inflation to fall gradually instead of hiking “until something breaks.”

More broadly, the authors note, many features of the pandemic downturn and subsequent recovery have been surprising and unique. Perhaps the endgame of this cycle will bring another surprise. For more information on this subject, please see Recession vs. Soft Landing: Is This Time Different? (12 Sept)

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.