An effective corporate climate change strategy for reducing emissions requires a detailed understanding of a company’s greenhouse gas (GHG) emissions.

Until recently, companies focused on emissions from their own operations under Scope 1 and Scope 2 of the GHG Protocol.

But increasingly, companies understand the need also to account for GHG emissions along their entire value chain and product portfolio.

Overview of GHG Protocol Scopes and Emissions Across the Value Chain |

|

|

|

Source: GHG Protocol |

Scope 1 emissions cover fuel combustion at company facilities, company vehicles and fugitive emissions.

Scope 2 emissions cover purchased electricity, heat and steam.

Scope 3 emissions cover all other indirect emissions that occur in a company’s value chain, and they are much more complex than the other two scopes for companies to disclose.

For a company producing trucks or cars that consume fossil fuel, for a bank with the majority of loans to fossil fuel and for all oil and gas explorers and producers, Scope 3 emissions are by far the biggest GHG emissions category.

Despite the challenges of addressing indirect emissions, Scope 3 not only has huge potential to prevent the worst impacts of climate change, it can also lead to substantial business benefits.

Companies can mitigate risks within their value chains, unlock new innovations and collaborations, and respond to mounting pressure from investors, customers and civil society.

The Fifteen Scope 3 Categories

|

|

|

|

Source: GHG Protocol |

Companies have been voluntarily disclosing Scope 1 and 2 emissions for a considerable time, most notably to CDP, a not-for-profit charity that is the gold standard of environmental reporting with the richest and most comprehensive dataset on corporate and city action. In recent years, CDP has requested Scope 3 disclosures, noting the challenges for companies with complex supply chains – hence the lack of data and inconsistency in reporting of data.

A number of benefits are associated with measuring Scope 3 emissions. For many companies, the majority of their GHG emissions and cost reduction opportunities lie outside their own operations.

Regulation Reduces Reporting Barriers

Scope 3 reporting and reduction is growing, enabling companies to mitigate risks within their value chains, unlock innovations and collaborations, and address mounting social pressure for such action.

Citi analysts say companies and their value chains need to work together and collaborate on reporting, calculation and estimation methodologies, and engage to identify and address potential double counting. Investors can also play a significant role in influencing Scope 3 disclosure among investee companies, enabling a more accurate and complete calculation of the carbon footprint of their portfolio, and the carbon risk it carries.

The following are commonly cited barriers to Scope 3 reporting:

- Data collection: Difficulties in capturing reliable data in a systematic and auditable fashion across the value chain, due to lack of direct control. Aggregated data (e.g., information reported to CDP) can be useful here for estimation purposes.

- Emissions factors: Difficulties selecting emission factors to derive accurate calculations.

- Supplier engagement: Challenges engaging with suppliers to both report and reduce emissions.

- Double counting: Value chains can overlap, with one company’s direct emissions potentially counting as the upstream and/or downstream emissions of others. Scope 3 emissions could be accounted for by several different companies.

- Responsibility: Scope 3 emissions by definition are outside of a company’s direct control. Further, differences in underlying business models, such as the use of outsourcing, can significantly change the balance of Scope 1, 2 and 3 emissions. This can influence a company’s willingness to commit to Scope 3 reporting and reduction, particularly if its balance of emissions falls largely in the Scope 3 category. Comparatively, companies whose balance of emissions lie in Scope 1 and 2 are disadvantaged by a focus on these categories alone.

Analysis of Scope 3 Country and Company Disclosures

According to CDP, companies that publish environmental data consistently and on an annual basis protect and improve their reputation, get ahead of regulation, boost their competitive advantage, uncover risks and opportunities, track and benchmark progress and get access to a lower cost of capital. In 2021, a record 13,000+ companies reported environmental data to the annual CDP questionnaire.

CDP highlight companies for their environmental leadership and 272 out of nearly 12,000 scored companies were recognized on CDP’s annual A List, demonstrating a significant improvement in the quality of their disclosures.

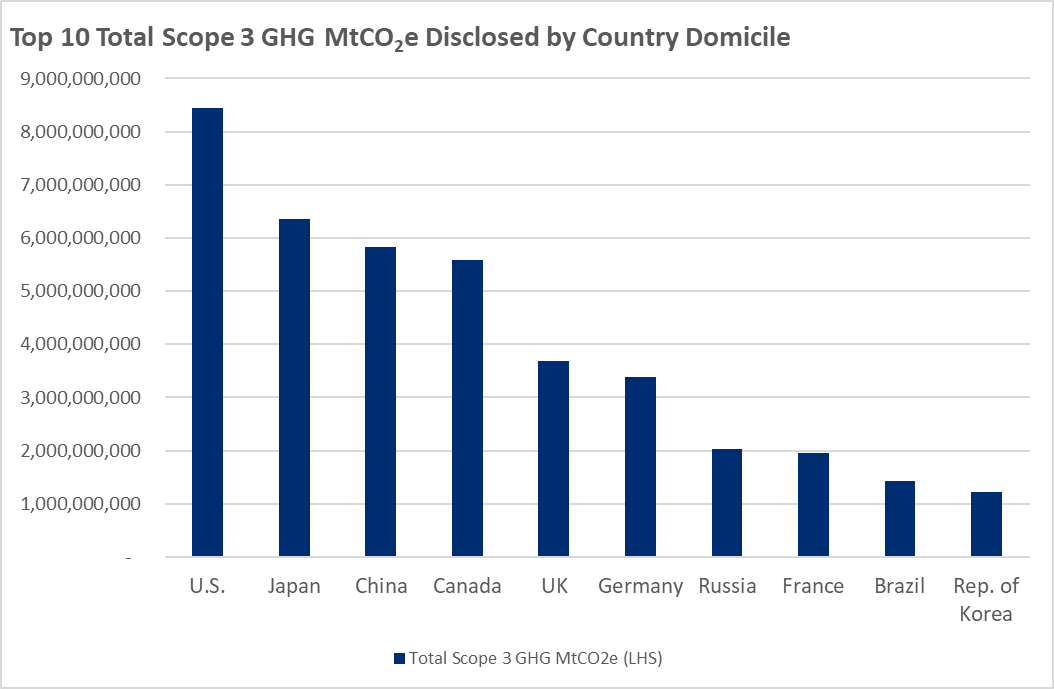

Total Scope 3 Emissions Disclosed to CDP by Country Domicile |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, CDP |

Citi analysts found that the U.S. has the largest amount of responding Scope 3 emissions identified by company domicile. Japan, China, Canada and the UK make up the rest of the top five. This reflects the country of domicile of a company and the willingness to disclose, along with future regulatory expectations.

The analysts looked at the proportion of companies that consider Scope 3 to be relevant and calculated it relative to the total number of companies that disclose to CDP. Although the U.S. has the largest volume of Scope 3 emissions disclosed, only a quarter of companies consider Scope 3 relevant and are calculating their Scope 3 emissions.

Japan has the second-largest Scope 3 emissions being reported by domiciled companies. Just over 45% of companies that report to CDP believe Scope 3 is relevant and are calculating and reporting Scope 3 emissions.

As global regulation on climate-related disclosures evolves from voluntary to mandatory, Citi analysts expect the percentage of companies calculating and disclosing on Scope 3 emissions to increase. Companies will begin to feel the pressure to disclose as regional and sector peers identify and report on value chain emissions.

More companies disclosing will make it easier to fill in data gaps from non-disclosing companies. This would likely provide further catalysts for Scope 3 disclosures as companies would generally prefer a more accurate depiction of their emission status.

And as companies disclose their Scope 3 emissions this exposes them to heightened scrutiny from key stakeholders such as shareholders, employees and consumers. This might result in further pressure to decarbonise at the Scope 3 level. For more information on this subject, please see Western Europe ESG & SRI - Understanding the Scope of Scope 3 Emissions and for further reading please also see this report by Jason Channell and team.

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.