The conflict in Ukraine has created supply disruptions across the commodity complex. Many believe the impacts are transitory. But in steel, the impacts could be more sustained as production capacity, especially in Ukraine, has been materially impaired. Post-conflict reconstruction will also require steel. The conflict is the latest in a litany of global supply chain disruptions, and could lead to a re-assessment of safety stock requirements, Citi analysts say. Localization of supply chains – arguably including steel production – is another impact of the disruptions.

The full Citi report provides background and context to the current situation and tries to quantify the impact of recent events on the steel markets.

The dissolution of the Soviet Union generated a wave of net exports which peaked at 56 million tonnes (c.18% of world steel trade) in 2004 but came down to 38 million tonnes (c.8% of world steel trade) in 2020. Post the Soviet dissolution, the demand decline was c.80% by 1997 but production declined only 54%.

China has since emerged as the big net exporter, and the importance of the former Soviet Union states as the key source of steel exports declined to c.8%. A big step-down in exports came post the 2014 Russia-Ukraine conflict, after which 10 million tonnes of production and exports went off the market and have not come back.

Ukraine could be a net importer of steel for the medium term but Russia could find its exports stranded. Press reports suggest two of the biggest steel mills in Mariupol – one of the world’s key steelmaking and exporting hubs – have been significantly damaged. That in itself could take out the 13 million tonnes per annum of steel Ukraine has been exporting for the medium term. The Kyiv School of Economics estimated damage to civilian and military infrastructure of $270bn as of early April. Using benchmarks from other emerging markets, replacing that amount of infrastructure would require 10-15 million tonnes of steel (~2mn tonnes/year if done over 5 years). Also Russia + Ukraine exports ~54 million tonnes of iron ore units in the form of iron ore, pig iron and scrap, which makes the ferrous markets significantly tighter.

Potentially 20-50mn tonnes (1-3%) of structural change in global steel supply-demand

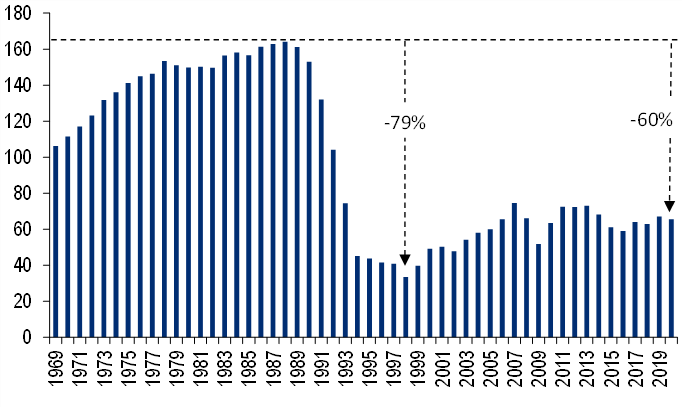

The USSR/FSU produced 160 million tonnes of steel per annum (c.20% of the world total) in 1969-1989. That collapsed to 77 million tonnes during 1996 (-54% vs the peak level a decade before).

Steel Production : USSR / Former Soviet States (mn tonnes/year) |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, World Steel |

It has recovered a little since, but was still around 100 million tonnes in 2021 (38% below the 1988 peak of 163 million tonnes). With the growth of China, the former Soviet Union countries account for only around 5% of global steel production.

Apparent consumption paints an even worse picture. Apparent consumption fell to 33 million tonnes in 1998, almost 80% lower than the 164 million tonnes peak in 1988. Even after the recovery to 65 million tonnes over the last few years, it is still 60% below the peak levels of 1988.

Steel Apparent Consumption: USSR / Former Soviet States (mn tonnes/year) |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, World Steel |

However, for world steel markets, production fell by less than supply. Exports from USSR/former Soviet states increased dramatically – from almost no net exports until 1990 to a peak of 56 million tonnes in 2004, and 35-45 million tonnes since.

Net Imports / (Exports) of Steel from USSR / Former Soviet States (mn tonnes/year) |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, World Steel |

The squeeze-up in steel prices during 4Q'20-4Q'21 was essentially driven by extreme lack of availability. The supply chain disruptions over the last 2-3 years are also triggering a review of safety stock requirements across the supply chain, Citi analysts say.

Quantifying the potential demand uplift from this 'paradigm shift' in terms of safety stock is unavoidably imprecise. Citi analysts have run scenarios for the system-wide steel inventories increasing by 10-70% over 1-5 years, as illustrated in the chart below.

Uplift in annualized steel demand due to increase in system-wide safety stock requirements (% increase in demand over 1-5 years) |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research |

The most likely scenario, according to the Citi team, is for a 20-30% increase in inventories over a 3-5 year period. This could result in a 2-4% uplift in annualized demand over the 3-5 year period, everything else being equal.

The steel market since 2017 has been dominated by trade protectionism. Global steel trade has declined by c.16% since the peak in 2016 to 401 million tonnes (including a 9%y/y decline in 2020, exacerbated by weak global demand). As a % of global steel apparent consumption, internationally traded steel constituted 22.9% of the overall consumption, down from 31.3% in 2016.

The outlook for global steel trade over the next decade also depends on demand growth as well as protectionism – it was the global financial crisis that led to a collapse in steel trade as traders got squeezed on liquidity and global growth slowed (trade tends to accelerate when global demand accelerates and decelerate when demand growth slows). In 2009 post the GFC, steel trade dropped 25%y/y even though steel apparent consumption fell only 7.5%y/y (and consequently steel trade as % of apparent consumption dropped to 28.6% in 2009 from 35% in 2008).

World steel demand has been in a slow recovery mode since and the rate of that recovery will play a big part in the quantum of global steel trade – in addition to protectionism. As transitory supply chain strains hit a range of commodities, steel looks to have particular challenges that may mean its supply strains persist longer term. For more information on this subject, please see Global Steel - Long-term impacts of the recent steel supply disruptions

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.