The Strive for 45 and the Role of Cheap Gas in the Energy Transition

KEY TAKEAWAYS

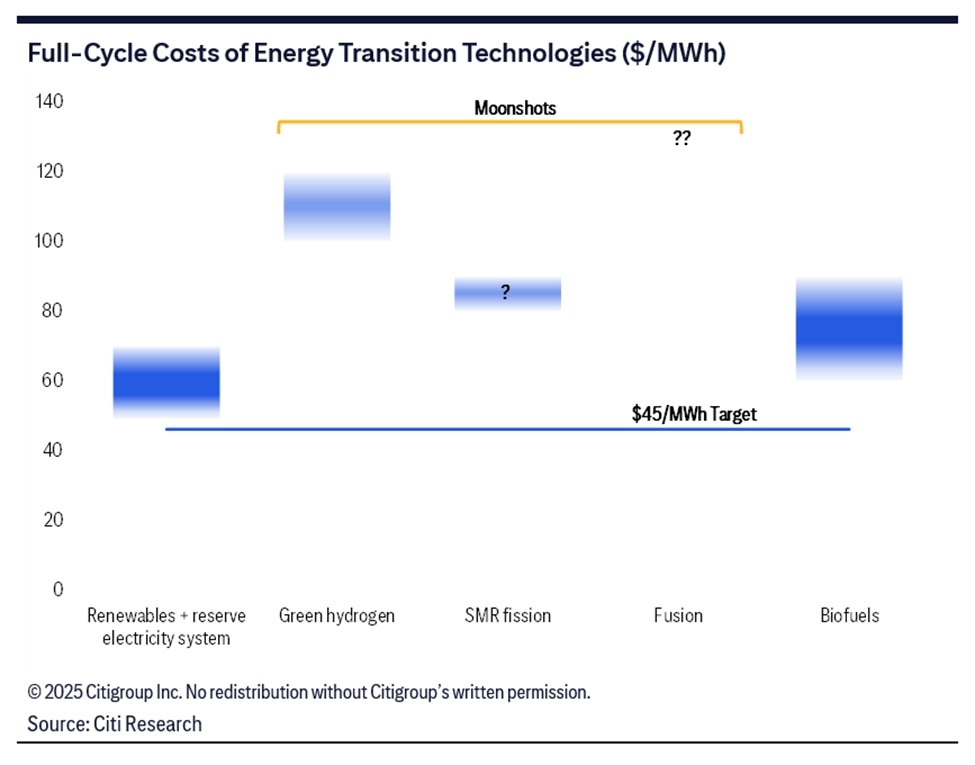

- We size up existing energy transition technologies to see if they can match the current energy system’s affordability target of $45 per megawatt-hour.

- A big challenge is that to meet seasonal swings in demand, renewables need to be combined with a backup energy system.

- We see cheap gas as key to delivering an alternative system, a boon for the U.S.

In a new Super-Sector Analysis, a team led by Alastair Syme, Global Head of Energy Research, looks at what an affordable Energy Transition might look like, setting $45 per megawatt-hour (MWh) as a target for affordability and sizing up energy technologies based on this reference point. Our conclusion is that access to cheap gas is critical for delivering an alternative to our existing energy system. Cheap gas looks to be a big asset for the U.S., and we believe it will emerge as a cornerstone of Trump’s 2025 energy policy.

The Energy Transition has become politicized, and in many respects that’s extraordinary: Why should the debate about “clean” seemingly divide along ideological lines? But it’s also not hard to see why it’s happened. The job of any industry is to deliver a cheaper and better product to consumers, and the Transition industry has delivered a product that’s “better” as in “low carbon” while failing to offer energy at a more competitive price than our existing global system. The divide is not really one around political ideology, it is one around affordability.

“The divide is not really one around political ideology, it is one around affordability.”

The closest affordable alternative to our existing energy system looks to be a combination of renewables (solar and wind) and a backup system of gas-fired power to meet seasonal swings in demand, though we emphasize this is only true in certain parts of the world. The target for affordability we’re using is a reference point of $45/MWh; in regions where renewables output is high and gas is cheap (such as Texas and the Middle East), we think a new system’s cost can get down to around $50/MWh.

Access to cheap gas is critical to affordability, and because of that we see the bounty of cheap U.S. gas emerging as a cornerstone of Trump’s 2025 energy policy. Technically recoverable gas reserves in the U.S. are estimated at more than 100 years of current production, and we think much of this would come at a price point not too far away from today’s low prices. The ability to use these reserves to provide flexible backup for renewables, or even as a baseload for powering AI data centers, is an opportunity few other countries have.

The “strive for 45” and current competitiveness

Media coverage of the Energy Transition often creates a picture of rapid change by focusing on selected elements of the Transition, when the discussion really needs to be a much broader one about the entire energy system.

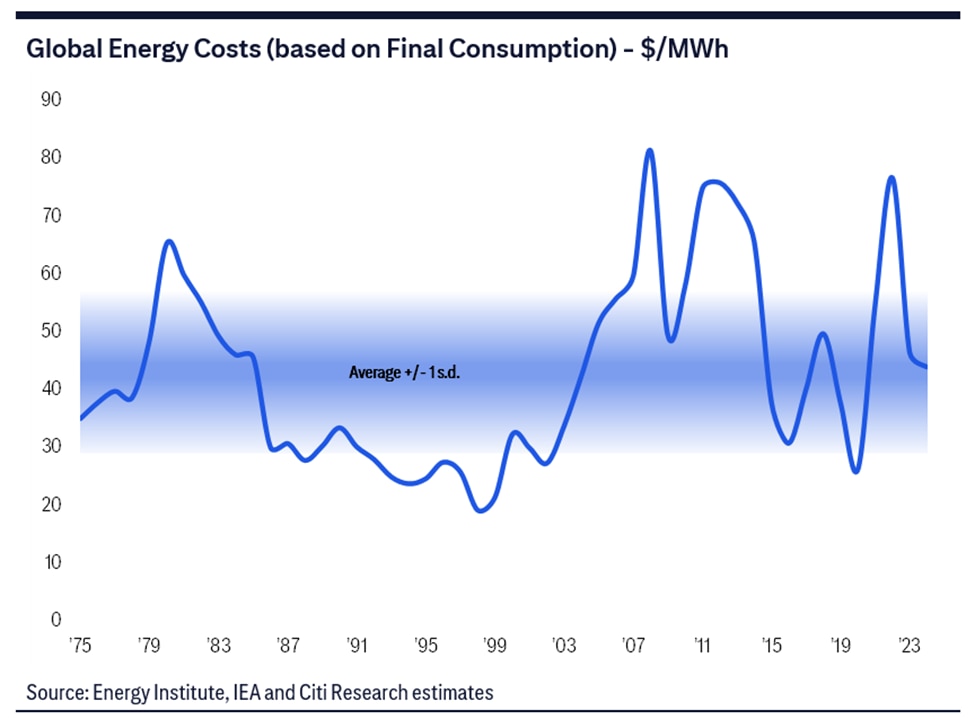

We estimate that some 83% of today’s global useful energy (the thing that heats, moves and powers society, after accounting for losses in energy conversion) is provided by oil, gas and coal. Another 5% comes from bioenergy and waste; the remaining 12% comes from hydro, nuclear, geothermal, solar and wind.

Our estimate is that global society is spending around $5 trillion a year on wholesale energy costs, though that number varies considerably year by year given swings in global oil, gas and coal prices. That equates to a price of around $45/MWh when measured against final energy consumption, giving us our reference price for further discussion. We argue that the competitiveness of Energy Transition technologies will be defined by their ability to match or beat this reference price.

So how cost-competitive are the major Transition energy technologies? We consider renewable energy (via solar and wind), green hydrogen, nuclear (fission and fusion), and bioenergy. We don’t consider hydro, as most practical large-scale hydro in the world has already been deployed. We also don’t consider geothermal energy, as from what we’ve seen the costs are still far from being competitive.

The conclusions of our technology run-through aren’t particularly encouraging. Renewables can be competitive in parts of the world, but generally only on an as-produced basis; they’re incapable of meeting the significant seasonal swings in demand most countries face. This need for seasonal backup capacity adds materially to the system cost, and means that cost-competitiveness will really be defined by where natural gas — the logical backup source for seasonal swings — is cheap.

Renewables and reserve

We begin with renewables and reserve. In parts of the world, renewables can be a low-cost source of energy. But there’s a huge range of prices, ranging from $16/MWh for utility-scale solar in the Middle East to above $130/MWh for recent purchase deals for offshore wind in New York. This range reflects a variety of factors that make comparisons difficult: technology, load (availability), supply-chain and construction costs, and the cost of capital.

Solar has proven the most cost-competitive technology, with gains coming from improvements in output but more fundamentally from deflation, led by China. The Middle East is at the bottom of the solar cost-curve due to ample sunlight, cheap land and a willingness to fully benefit from the supply-chain deflation. A key question for the U.S. and Europe is whether there’s the political will to continue to embrace deflation, or if governments will turn to protectionist tariffs that could slow solar investment. Tariffs on Chinese solar equipment certainly look like a possibility in the U.S.

The world is installing 2.5 times the solar capacity it did in 2020, but wind installations are expanding at just 1.2x. Arguably wind is where the renewables industry got inflation wrong, working on the premise that prices would continue to drop when in fact technological progress has stalled, with turbines no longer getting bigger, and the supply-chain has struggled to return a profit. As with solar, a pathway to deflation looks largely dependent on the political will to embrace the Chinese supply chain, where costs are 30% cheaper.

Assuming real weighted average cost of capital of 6% to 7%, achieved through 80%+ debt financing, the full-cycle costs of solar and onshore wind in places such as Texas, southern Europe, parts of China and the Middle East can match or undercut our $45/MWh reference price. But that’s on a “when-produced” basis, and the inherent problem of renewables is that they’re intermittent over both the short and long term.

Short-term intermittency (such as during the day or week) can be resolved using batteries, other storage methods or smart grids. But these solutions can’t meet the challenge posed by seasonal variation. The solution for long-term storage, which we call “reserve,” has to be something that provides much higher energy density and deliverability, which makes this a debate about gas, coal and nuclear. Gas offers low upfront capital costs and high operational flexibility, making it easily the best candidate of the three.

The intermittency issue is different in different places. In Texas, renewables meet about half of winter demand, and it’s possible to imagine a future in which they scale to 100% of that demand. But Texas demand in summer is 1.7 times that seen in winter due to air conditioning.

It would be nonsensical to build renewables to meet summer demand, as you’d have overcapacity for half the year. Texas’s strategy has been to meet higher summer demand with gas; it’s formed a $5 billion state government fund to provide loans for new gas-fired power generation, helping builders of these facilities overcome the economic challenge that comes with this capacity only being needed as reserve.

In Germany, renewables are already well on the way to meeting a large part of annual power needs. But there the demand peak is in winter, not summer, and a lot of current winter energy needs are met by gas. Decarbonization plans to replace gas heating with electricity (i.e., heat pumps) would push winter power needs to more than twice that seen in the summer.

Texas renewables look to fall in the range of $35/MWh to $55/MWh, but there’s the need to meet a 70% hike in demand for around half the year. This reserve capacity will need power prices of at least $50/MWh to make a return. In theory this means the entire system cost is also a little more than $50/MWh.

In Germany renewables are in the range of $50/MWh to $70/MWh. Here we need reserve to meet winter demand that’s two to three times what’s seen in the summer. Germany also faces much higher gas prices. All told, the overall system cost is at least $65/MWh.

Green hydrogen

What about parts of the world such as the Middle East that can offer much cheaper renewable power? Could we overbuild renewables in these locations and then export the energy? This is where governments in Europe, South Korea and Japan see a role for green hydrogen.

Hydrogen is a store of energy, but unfortunately, it’s rarely found in its pure form. The key cost of hydrogen supply is the energy required to break its bonds with other molecules: Getting hydrogen from water through electrolysis, for instance, sees 30% of the energy lost in breaking the bonds. Electrolysis, compression and transport push the costs of exporting green hydrogen into Europe or Asia above that of gas. Getting hydrogen prices to a level where they’d be a truly economic alternative essentially needs zero-cost renewables. Even if that were achievable, it would raise the question of whether the system would be better off consuming that energy as electricity rather than converting it to chemical energy for export.

Put differently, if countries such as Germany are adamant that their industry needs to run on green hydrogen, it might be better to relocate that industry to the Middle East and allow finished goods to be exported instead.

Fission and fusion

Nuclear fission as a power source for North American AI data centers was a key narrative in 2024, but we struggle to see cost-competitiveness at scale. Bringing a few mothballed assets back to life has little to do with new-build economics, which is what we think needs to be the center of discussions.

The Energy Department estimates the full-cycle cost of the most recent plant built in the U.S., Georgia’s Vogtle facility, at $126/MWh, but it’s closer to $200/MWh if adjusted for 2024 supply-chain and borrowing costs. The inherent expense of large-scale fission power reflects build cost and time, with operational safety the obvious priority, and nuclear isn’t good at scaling utilization up and down, so it doesn’t offer the same seasonal versatility as gas.

Some pin hopes around Small Modular Reactors (SMRs), but as yet the price point of this technology is unproven. The Energy Department theorizes prices could be as low as $60/MWh, but the cancellation of a potential project in Utah at the end of 2023 came amid cost analysis suggesting prices of $90/MWh, even after significant federal benefits and tax credits. The Energy Department’s lower cost-analysis appears to come from a view that adoption of SMR technology can shrink construction costs and build times as the supply chain develops. But how do you get to this point given the economic uncertainties?

As for nuclear fusion, we estimate that some $7 billion has been raised for private projects, giving rise to the idea that the industry is on the cusp of economic breakthrough. But in our view, fusion is still a science project.

Bioenergy

Bioenergy refers either to biofuels made from crops or waste products that can be blended into gasoline, diesel and kerosene or to biogas, generally methane used for power generation. The bioenergy industry has a lot of political support in the U.S., Brazil and Europe. We estimate bioenergy now provides 1.1% of the global energy supply, with four-fifths of that through biofuels; roughly speaking, we estimate bioenergy is now an $80 billion a year industry.

But anyone who looks at the industry will quickly appreciate the complex web of incentives and mandates that drive demand, with this market structure simultaneously the industry’s basis and its failing. The bioenergy industry seems to rely on more and more layers of incentives, which we think illustrates the cost challenges it faces.

The basic problem is that bioenergy’s base foodstocks have a substantial cost disadvantage vs. hydrocarbons: Crops such as corn, soybeans or sugar cane have an energy density that’s at most 55% that of gasoline and diesel. That’s why Brazil and Indonesia lead the world in biofuels penetration: Conditions there are conducive to high crop yields that help offset the problem of low energy density.

We estimate that bioenergy, on an unsubsidized basis, provides energy in a range of $60/MWh to $170/MWh. Because of this inflationary expense, policymakers try to reserve bioenergy’s use case for its most valued purpose: Especially for advanced biofuels, that use case is around jet fuel, as this industry has no other practical route to decarbonization and so can get the most value from bioenergy.

The problem with an industry based on incentives and mandates is policy risk. Currently, sustainable aviation fuel runs at a hefty 3x premium to traditional jet fuel. Europe’s current answer to this problem is to keep blending mandates very low (2% in 2025) so consumers won’t notice the additional cost. But those mandates are set to rise to 35% in 2035 and 40% in 2040. If costs haven’t come down considerably by then, consumers will notice, and we suspect political support will wane.

Our new report, The Strive for 45 and the Role of Cheap Gas in the Energy Transition, also includes a look at opportunities for energy investors. It’s available in full to existing Citi Research clients here.