As the ECB embarks on its rate hiking cycle, say Citi analysts, the inflation rates that the central bank can actually influence will be driven not by commodity prices and supply-chain disruptions but by the domestic labour market.

The extent of rate hikes will depend on wage growth. But also GDP growth will depend on whether households can eke out positive real income growth in 2023.

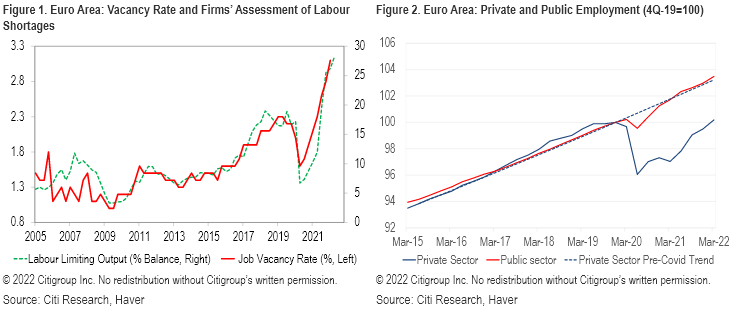

Latest Eurozone employment data continue to show a strengthening job market. In 1Q-22, employment was up by 0.6% QQ, and 1% above the pre-pandemic 4Q-19 level. Hours worked rose by 1.3% QQ (albeit still 0.6% below 4Q-19). While companies are still managing to fill positions, labour shortages are intensifying – the vacancy rate in 1Q reached a new historical high (of 3.1%) and so did the share of businesses reporting scarcity of labour as a limiting factor for output in 2Q – see Fig 1 below.

Widespread shortages may seem somewhat difficult to reconcile with the evidence that employment has returned to pre-pandemic levels, but not really to the pre-pandemic trend. This looks even more obvious for private-sector employment – see Fig. 2 below.

The full Citi report explores three potential explanations:

1. Cross-sector shortages

Even if on aggregate demand for labour does not overtake supply, shortages in certain sectors can still emerge due to skills/location mismatches, cross-sector re-allocation or inefficient labour markets, for example. The gap to the pre-pandemic trend is unevenly distributed across Eurozone economic sectors.

The biggest labour shortfalls are in the trade, travel, tourism and entertainment sectors – the industries arguably most affected by health restrictions during the pandemic – but also in manufacturing – which could reflect production disruptions but also structural trends, says the Citi report.

The narrowest gaps are in public-sector employment, but also in construction, IT, finance and professional activities (accounting for 50% of jobs).

2. Supply issues I: people working fewer hours

Supply of labour input may be impaired if people choose to work fewer hours. Hours worked have lagged behind employment by some margin. Output per hour is back to the pre-Covid trend while output per employed person is significantly lower. This is not unusual in post-recession periods – it took about one year after the GFC to close this gap. And hours worked per capita were already on a mild downtrend even before Covid, likely reflecting changing preferences. But the gap now is unusually large.

3. Supply issues II: outright reduction in the number of people available to work.

Unlike in the U.S., participation rates in the euro area do not suggest wholesale departures of workers from the labour market – they are already above pre-pandemic levels. However, Eurozone working-age populations have been shrinking for a while and the pandemic seems to have accelerated that trend, probably mostly due to less net immigration but also due to fast-ageing populations.

For more information on this subject, please see European Economics Weekly: Where Have All the Nice Workers Gone?

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.