June Chart of the Month: Equity market reading countervailing signals.

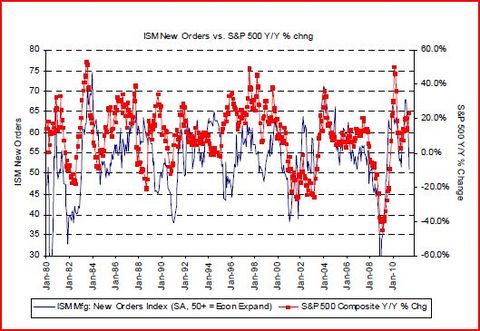

Industrial data matters for S&P 500 performance. The Institute for Supply Management (ISM) new orders index has been tightly correlated with the performance of the S&P 500 over the years and that relationship has tightened up even more in the past decade. Thus, given the slippage of the new orders numbers, it should not be shocking to investors that stock prices were vulnerable. Indeed, in an April note, we had noted that the new orders index looked stretched earlier this year and seasonal factors also could be problematic.

Source: Haver Analytics and CIRA - US Equity Strategy

Source: Haver Analytics and CIRA - US Equity Strategy

Yet positive news on credit conditions suggests that a new downturn is not emerging. Surveys from both the Fed and the National Federation of Independent Business argue fairly convincingly that it is easier for corporates (large and small) to access credit, though uncertainties about taxation, regulation, health care costs and budget deficits appear to be weighing on management decision-making. Nonetheless, if cost of capital remains so low, one should expect business investment to bounce higher since the return on capital exceeds the lowered hurdle rates.

In the mid and late 1990s, stocks and new orders acted asymmetrically. The tech bubble that began in the mid-1990s and took off again post Long Term Capital Management partially due to the Fed's liquidity kicker allowed for the equity market and the ISM to de-link. Our sense is that fears concerning a social media IPO bubble overstate a potential recurrence of that development.

NOTE: This post is adapted from Citi North America Equity Strategy's "June 2011 Chart of the Month," published on June 6, 2011.