Equity Strategy: August 2012 Chart of the Month

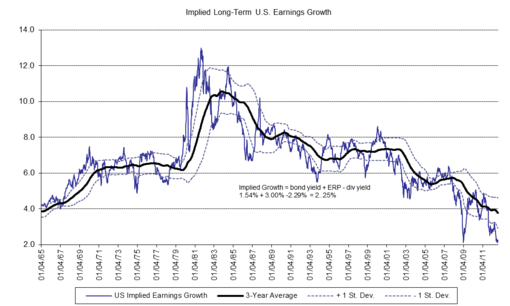

It is often worthwhile to gauge market expectations by assessing the long-term average equity risk premium and compare the expected return from stocks versus bonds. This approach allows one to consider very long-term expectations, recognizing that at any point in time investors may demonstrate extreme risk aversion or tolerance. In this context, the investment community has retreated back to its Great Recession anxiety because long-term earnings expectations appear to be matching late 2008/early 2009 lows.

{kind=link}

Bear arguments have shifted reflecting seeming rigidity over required flexibility. Fascinatingly, market bears first argued a recession was imminent last September which proved inaccurate; then, the contention shifted to P/E multiple contraction due to margin compression when the opposite typically has been true. Most recently, the current rally has been pinned on alleged Wall Street hopes of a Romney victory in November and QE3 expectations as if Mario Draghi's statements last week had no impact nor did earnings beats thus far in the second quarter reporting season.

When investors ignore what is seemingly priced into the market, finding fault becomes the "go to" method but does not change reality. Pundits tend to opine about possible rather than definite future trends without necessarily running analysis on what is embedded within stock prices. Metrics such as intra-stock correlation, the Citi Economic Surprise Index and earnings estimate revision momentum are far more instructive on near-term market swings than such potentially faulty forecasts, if history is any guide.