The Global Outlook Hinges on U.S. Performance

We continue to project softening in the U.S. around mid-year as the Fed struggles with hotter-than-expected inflation prints. We see the uncertainties surrounding the U.S. outlook as unusually pronounced, and their eventual resolution as a critical hinge point for the global outlook.

In our latest global economic forecast, Chief Economist Nathan Sheets and team see this year’s global growth settling in at a little under 2.5%, just a notch softer than last year’s pace, with the underlying economic processes staying strikingly similar to what we’ve seen in recent years. Strong consumer spending on services, along with tight labor-market conditions, continue to be growth’s principal drivers. While our forecast has envisioned a rotation back toward goods spending, so far any rebound in the goods sectors looks to be “green shoots” at best, with the drivers of growth not yet having shifted appreciably.

The good news is that key parts of the global economy have continued to show resilience despite numerous challenges including elevated geopolitical risk. Emerging-market economies look like they’re on track for another solid year, with their aggregate growth rate hovering near 4%, similar to 2023.

For the developed-market economies, we see an aggregate slowdown in growth this year, largely reflecting a projected U.S. deceleration around mid-year. More generally, how the U.S. performs strikes us as a hinge point for the global outlook. Given the U.S. economy’s size and reach, this is always true to some extent, but the uncertainties and implications around that performance seem particularly marked at present.

A Rotation Back to Goods?

Coming out of the pandemic, consumers rotated strongly toward services as they sought to make up for experiences they’d postponed. As the pandemic moves further into the rearview mirror, we’ve expected a rotation back toward goods. But any moves in that direction are still tentative at best.

The global manufacturing purchasing managers’ index (PMI) has crept slightly above 50, the breakpoint between expansion and contraction. We see a strong global bid for sophisticated AI chips, and the manufacturing inventory cycle looks to have become less of a headwind. But the electronics sector as a whole has yet to pick up appreciably, and PMIs for manufacturing orders and global exports remain lackluster.

After declining through the middle of last year, the services PMI has recently rebounded and points to solid performance. In addition, global services inflation remains comparatively hot, another sign of sector strength. Although the data have been uncooperative, we maintain our call for a rotation from services spending back to goods as the year progresses.

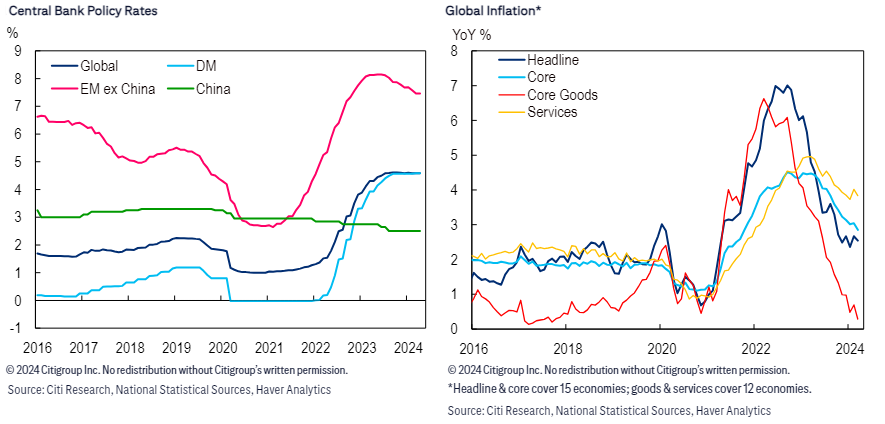

Further Global Slowing?

For some time, we’ve envisioned a more pronounced slowing in the global economy, which was expected to arrive due to the anticipated moderation in services spending taking some heat out of growth and the labor market, as well as headwinds from the substantial accumulated monetary tightening. And we have seen some effects: Global growth has remained below its 3% historical trend, both headline and core inflation have retreated, and some regions have felt significant drag from central bank tightening.

Even so, we expect some policy restraint still in the pipeline will manifest itself as the year progresses. The upshot would be a step down in aggregate consumer spending, with an accompanying softening in global labor markets, wage growth and services inflation. While we’ve seen some preliminary signs of this, labor markets clearly remain tight. In our view, further adjustments in the economy will be needed to bring global inflation down to central banks’ targets.

U.S. Scenarios and Their Implications

We think the prospects for the global economy through the rest of 2024 depend critically on U.S. performance, with the U.S. trajectory affecting the global picture directly due to its large share of global activity but also indirectly through, for example, the implications for other central banks.

We offer two scenarios for the U.S. economy, and some implications. Our first scenario is broadly consistent with our baseline forecast, while the second is more closely aligned with current consensus views and market pricing of central banks’ policy paths.

In our first scenario, the U.S. economy softens to a recessionary or near-recessionary pace. This prompts the Fed to start its easing cycle sooner and more aggressively, with four cuts during the second half of the year. The Fed’s rationale for cutting rates would be two-fold: to ensure the softening doesn’t proliferate or become entrenched; and because economic slowing would give it greater confidence that inflation was poised to fall back to the 2% target.

Such cuts would greatly simplify the lives of central bankers at the European Central Bank (ECB), the Bank of England, and the Bank of Japan. The ECB and the Bank of England would likely cut rates in tandem with the Fed, while the Fed’s easing would take some heat off the yen and, thus, reduce pressures on Japan to tighten.

In our second scenario, U.S. growth moderates from the rapid pace we saw in last year’s second half, but continues at a solid 1.5 to 2% rate. In sync, inflation gradually falls and the Fed cuts twice — once in the fall and again in December.

This scenario would pose more challenges for other central banks than our first one. To the extent that the Fed remains on hold awaiting evidence of disinflation, it highlights the question of whether — and to what extent — other central banks are willing to go their own way in cutting rates.

The ECB has clearly signaled that it’s prepared to cut in June, which strikes us as essentially a done deal. A Fed that held rates would complicate President Lagarde’s efforts to manage her committee and create complexities for ECB communication, with concerns about a weaker euro also possible. In such a situation, the pure economic case for cuts would need to be compelling. Meanwhile, Japan’s policymakers would continue to fight yen appreciation with an eye toward eventual Fed cuts.

Other scenarios are possible, of course. For example, U.S. inflation could be sufficiently sticky that the Fed doesn’t cut at all this year or, in an extreme case, is forced to hike. This would amplify the challenges facing other central banks and, in our view, further raise the bar for them to cut rates.

Our new report, Global Economic Outlook & Strategy: The Global Outlook Hinges on U.S. Performance, also includes country-by-country discussions. It’s available in full to existing Citi Research clients here.