A new report from Citi Research’s chief economist Nathan Sheets says the probability of a more severe, synchronized global recession is now 30%, down from the 50% in the second half of 2022.

Recession Forecasts

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission.

Note: Arrows indicate recessionary periods; light blue indicates no recession.

Source: Citi Research

Recent weeks have seen a dynamic transition in the global economy, marked by China’s abandonment of its zero-COVID policy. It’s also been unexpectedly warm and windy in Europe this winter, allowing natural gas storage levels to stabilize.

That’s not to say 2023 will be easy. It won’t. But these recent developments mean the possibility of a “less hard” economic landing looks to have risen.

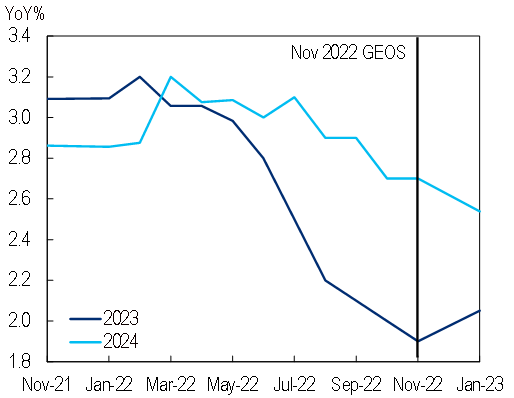

Citi Research estimates that global growth recorded a near-trend 2.9% performance in 2022, and expects the pace to ease this year to just 2.1% as economies around the world face pressure from high inflation and restrictive monetary policy.

Global Growth Forecasts

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Citi Research

In 2024, Citi Research expects a rebound in global growth to 2.5%. At the country level, Citi analysts expect recessions in the euro area, the U.K., the U.S., Canada, and many emerging markets—though it now expects Germany to narrowly avoid one.

Headline inflation is seen declining slowly to 5.6% this year and falling more convincingly to 3.7% in 2024.

Growth in many economies will be meaningfully below trend if not recessionary as central banks keep policy tight.

Oil prices to remain well contained, and for food price inflation to likely come down from high levels. Those factors look sufficient to keep headline inflation declining.

Core inflation, however, is a more difficult question. With the pandemic broadly in retreat, consumers have switched from goods spending back to services, leading to decelerating goods inflation but increasing services inflation. Services pressures are likely to persist, and because services are relatively labour-intensive, the rotation to services has meant increased demand for workers and upward pressure on wages. That will keep central banks on high alert.

The team sees the Fed continuing to hike rates in the first half of 2023, pushing rates well into the 5% range.

Meanwhile, the ECB is expected to raise the deposit rate another 150 basis points to 3.5%.

Three Closer Looks

The tone of recent developments in China, the euro area, and the U.S. is more positive than the team had anticipated, though all three economies still face significant risks and challenges.

China’s retreat from its zero-COVID policy came more quickly and proved more far-reaching than the team had anticipated, and while that implies a challenging near-term surge in COVID cases, early evidence suggests that the economic disruptions may prove manageable.

The euro area has seen surprisingly benign developments of late, prompting Citi to raise its 2023 growth forecast to 0.6%, a swing from a forecast loss of 0.4%. The most positive development has been warm, windy weather.

In the U.S., recent data have pointed to surprising resilience. Citi now estimates that the economy grew 2.6% on an annualized basis in the fourth quarter, while inflation indicators look to have moderated.

For more information and a full rundown of Citi Research’s latest thoughts and economic forecasts from around the world, please see Global Economic Outlook & Strategy - A “Less Hard” Landing Ahead?

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.