As covered in its recent report, the team expects recessions are in the cards for important world economies, but sees the timing as varying, depending on each economy’s underlying momentum and exposure to global shocks. For example, high natural gas prices and lagging real wages are likely to push the euro area into recession beginning late this year, while the U.S. economy’s greater momentum should keep it out of recession until the second half of 2023.

The Bad News: Inflation Is Driving Rate Hikes

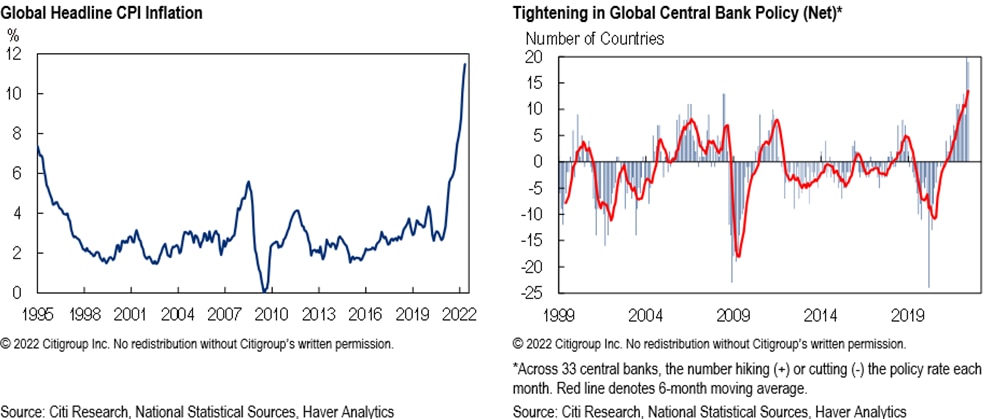

These economies face broadly similar pressures. Global headline inflation is running at its hottest pace in decades, which has prompted central banks to raise rates in the early stages of the most concentrated tightening campaign seen in more than 20 years. And global economic activity remains hampered by both pandemic challenges and stresses from the Russia-Ukraine conflict, with Russian gas supplies to Europe of particular concern.

But the authors note that these forecasts must incorporate a competing dynamic: China, where Citi Research recently reiterated expectations for 3.9% growth this year. Economic data show mounting evidence of recovery, and the government is likely to implement stimulus measures. Those measures should drive a second-half rebound that sets the stage for strong growth in 2023, when Citi Research also expects China to revisit its zero-COVID policy. Taken together, these factors have prompted the economics team to boost its China growth forecast for 2023 to 6.1%, up from 4.8%.

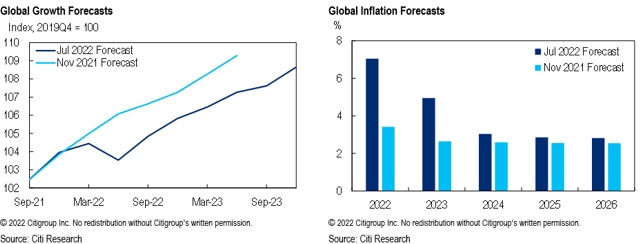

Pulling together these developments, the current forecast envisions global growth of 2.9% this year and 2.5% next year. These projections have been reduced by 0.1 percentage point in 2022 and 0.3 percentage point in 2023. Excluding the stimulus-related mark-ups in China, the projections for global growth next year are down by 0.6 percentage point, including a sharp 0.8 percentage-point cut for developed-market economies. In sum, since the end of last year, Citi Research economics has reduced its 2022 and 2023 global growth forecasts by 1.3 and 0.7 percentage points, respectively. At the same time, it has raised its inflation forecasts by 3.6 and 2.3 percentage points, respectively.

Such sizable revisions underscore the devastating supply shocks that have been seen, and the headwinds—from Omicron to the Ukraine crisis and high commodity prices—that the global economy has faced. By any metric, the authors note, the global economy is slowing—and its prospects are deteriorating.

The Good News: Recessions Should Be Mild

On a more positive note, generally speaking Citi Research expects recessions to be relatively mild and to occur in sequence rather than all at once. Those factors should allow the overall global economy to avoid a full-blown downturn.

“Global recession is, indisputably, a clear and present danger.”

However, the authors observe that the risks to this forecast are skewed significantly to the downside. They note that global recession is, indisputably, a clear and present danger, and projected downturns in a number of major economies underscore the point that these risks have become more concrete over the past month.

The global economic environment is challenging, and risks abound. The economists caution that the downturn could prove more synchronized than they are projecting—for example, if recession in the euro area triggers a loss of confidence and a broader global contraction, or if Russia cuts off gas supplies to Europe. Slower growth could undermine confidence and kick off “stall-speed” dynamics that cause a sharper drop in growth. And the team admits they are painfully aware that 2022’s revisions to their forecast have been almost entirely one-sided—with growth estimates moving steadily lower—and they can hardly be confident that the current forecast marks the end of such revisions.

Global recession is, indisputably, a clear and present danger.

Ease in Supply-Chain Pressures Could Defuse Inflation

In debating the probability of recessions, the authors note the need to consider an important change in the global economy—the softening in consumer demand for goods.

They see two factors driving this softening. First, during the pandemic consumers opted for goods and not services. Now that people are feeling more comfortable with COVID risks, the balance is tipping back towards services. But at the same time, rising prices are cutting into real incomes—a dynamic that strikes Citi as more threatening.

With goods demand slowing, global supply-chain pressures have eased: In June, the Citi Research Global Supply Chain pressure index showed its first meaningful retreat since January. But this is hardly an “all clear” signal for supply chains, the economists warn. Many risks are still in play, from the possibility of further manufacturing disruptions to the wildcard of the Russia-Ukraine conflict.

And to take a broader perspective, the team notes that the effect of softer consumer demand on their recession scenarios isn’t clear. Easing supply-chain pressures could help defuse inflation and lessen the pressure on central banks to raise rates. But slower consumer demand for goods could also indicate broader risks to consumer spending, with the chance of a further squeeze in real incomes. Which of these effects will prove dominant? Unfortunately, there’s no way to know yet.

For more in-depth analysis, please see Global Economic Outlook & Strategy – Global Recession—A Clear and Present Danger

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research. The comments expressed herein are summaries and/or views on selected thematic content from a Citi Research report. For the full CGI disclosure, click here.