Critical Minerals and the Question of Energy Security

Critical minerals are becoming more critical.

With energy security and the need for resilient commodity supply chains in the spotlight, critical minerals have emerged as a vital component in the energy transition, due to the role they play in numerous clean energy value chains.

The ability to access and use these resources efficiently is key to ensuring these minerals do not become the next energy security crisis in the global effort to achieve net zero.

The global supply of these critical minerals- such as lithium, nickel, cobalt, manganese and zinc- has historically been dominated by a select few resource rich countries including South Africa and Democratic Republic of Congo.

The midstream and downstream segments- that is refining/making useful and control of that supply- has largely been dominated by China.

Increasing demand to mine critical minerals looks like it will continue to be driven by:

- Growing demand for Electrical Vehicles linked to demand for lithium, nickel, cobalt, manganese and graphite

- Increasing demand and usage of wind energy linked to demand for copper, nickel, manganese, chromium and zinc

- Increasing demand and usage of solar energy linked to demand for copper and silicon

- Regulation

Current production and processing dynamics will change and adapt with growing demand. And regulation will play a key role given there are approximately 200 pieces of policy and regulation from 25 countries and regions worldwide, over 50% of which have been introduced in the last couple of years.

Several governments are looking to create environments backed by incentives for companies to improve critical minerals output across the value chain.

Also, the quest for energy and climate security has fostered greater focus by governments to attain supply chain independence and resilience.

U.S. Inflation Reduction Act (IRA)

The much-debated U.S. Inflation Reduction Act (IRA) reiterates the importance being placed on securing critical mineral supply chains in the U.S., with strong incentives to promote domestic production.

With US$369 billion earmarked for investment in energy security and climate change projects, The Act contains critical mineral investment incentives. To comply with the consumer tax credit for electrical vehicles, critical minerals must be extracted or processed in the U.S. or in any country with which the U.S. has a Free Trade Agreement (FTA) in effect or recycled in North America. Current critical minerals producers with FTAs include: Australia, Chile, Mexico and Canada.

At least 40% of the critical minerals used need to be developed or built in North America from 2024 and this threshold increases to 80% in 2026.

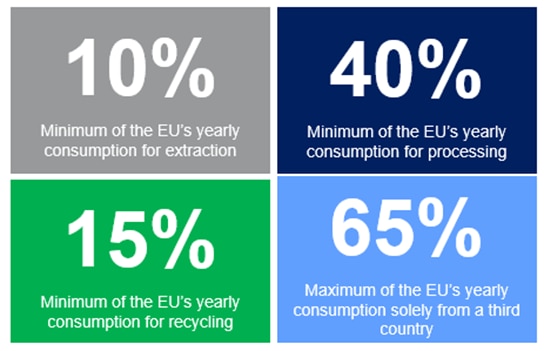

European Critical Raw Materials Act

Similarly, the European Union is dependent on international trade for its critical minerals supply requirements. With such high concentration risk, the Critical Raw Materials Act seeks to reduce the supply concentration risk and maintain global competitiveness, especially considering the stimulus outlined in the U.S. Inflation Reduction Act.

In line with the objective to build more sustainable and self-aligned supply chains, The European Critical Raw Materials Act has set target benchmarks for domestic capacities.

European Union Critical Minerals Act Target Benchmarks

Source: European Commission

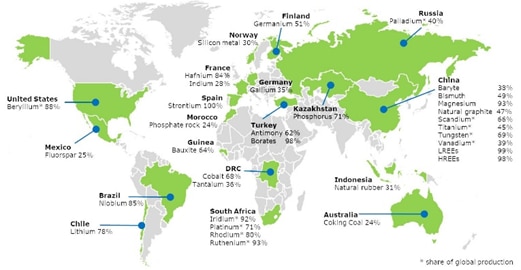

Critical Mineral Top Producers

The chart below highlights the countries considered to be top producers in different critical minerals. As indicated, China is a major player in the supply of critical minerals, standing out as a top producer of various critical minerals such as Magnesium, Scandium and Titanium. China also dominates the market in critical mineral processing, in the midstream and downstream segments of the market.

Top Producers of Critical Minerals

Source: European Commission

The research note seeks to emphasize the linkages between the energy transition, climate security and the supply of critical minerals. To successfully fulfil net zero ambitions and attain climate security production of critical minerals need to be accelerated to fulfil the resulting increasing demand.

Critical Mineral Demand

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Citi Research, IEA

The chart above highlights mineral demand under both the Stated Energy Policies Scenario (STEP) and Sustainable Development Scenario (SDS) scenarios. In both 2030 and 2040, there is a significant disparity between both scenarios, with the STEP scenario indicating lower demand than the SDS scenario by 36% and 65% respectively.

The gap between the two scenarios arguably suggests anticipated demand growth by governments and organizations for critical minerals is lower than the actual requirement to achieve climate goals. This could potentially lead to consequences such as increased prices of critical minerals beyond already projected forecasts.

As a result, input costs for clean energy technologies could also face inflationary pressures which translates to a more costly energy transition. Across the value chain, companies operating within the midstream and downstream segments would be largely impacted, whilst producing companies in the upstream segment would benefit from increased prices of the minerals.

Critical Minerals Investment Gap 2022 – 2030

© 2023 Citigroup Inc. No redistribution without Citigroup’s written permission.

Source: Citi Research, IEA

According to the IEA, the required investment in critical minerals is between US$360 billion and US$450 billion. Taking the announced projects into account, the current investment gap is 54%, or US$194 billion - US$243 billion. The mineral currently with the largest investment gap is copper, with 36%, followed by nickel with 16%.

For more information on this subject, please see Global ESG & SRI - Critical Minerals – The Next Energy Security Crisis? (12 June)

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.