The market for carbon credits has grown steadily in recent years. Now it looks poised for a period of rapid expansion as companies embrace carbon offsetting in huge numbers. A new report by Citi’s Francesco Martoccia takes a deeper look at the market’s fundamentals and potential.

The global market for carbon credits could be on the cusp of spectacular growth. Citi analysts estimate the market value of international and independent carbon credit markets doubled last year to over $1 billion. And they say that depending on price trajectory, increasing supply and demand of carbon offsets could boost the size of the market to $50-to-over $100 billion by 2030.

The estimate comes as new regulations force more companies to abide by established obligations or voluntarily adopt stricter environmental targets. Furthermore, COP26 has paved the way for the establishment of a global carbon emissions market through marketing of carbon offsets.

The market for carbon credits first sprang up in the 1970s but failed to ignite amid doubts about greenwashing and structural imbalances. In more recent years it has made a comeback as market participants increasingly recognize its pivotal role in addressing climate change.

Through 2021, cumulative issuance and retirements of independent carbon credits outpaced any other year on record, close to 300Mt and 120Mt respectively. The U.S. was home to most of the buyers of carbon credits, followed by Western Europe. Financial institutions and big oil were the most active buyers of carbon credits, accounting for 25% and 20% of the total retirements, respectively.

Indeed, offsetting unavoidable emissions through a carbon crediting market may be a reasonable alternative to facilitate and ensure the undertaking of actions toward decarbonization by hard-to-abate industries.

There is no unique price for carbon credits, as each transaction differs due to idiosyncratic factors such as the preference of the market participants for specific registry standards, the vintage year (see later explanation) of the carbon credits, the size of the transaction itself, the geography and the category of the projects.

Most future supply of carbon offsets is likely to originate from nature-based projects over the next ten years, absent technical innovations in carbon sequestration. Nature-based solutions account for 40% of the cumulative issuance of carbon credits at present. Furthermore, nature-based solutions are among the most cost-effective pathways on a $/Mt CO2 basis, outside of hybrid natural-engineered solutions, whose technology is yet to be fully employed.

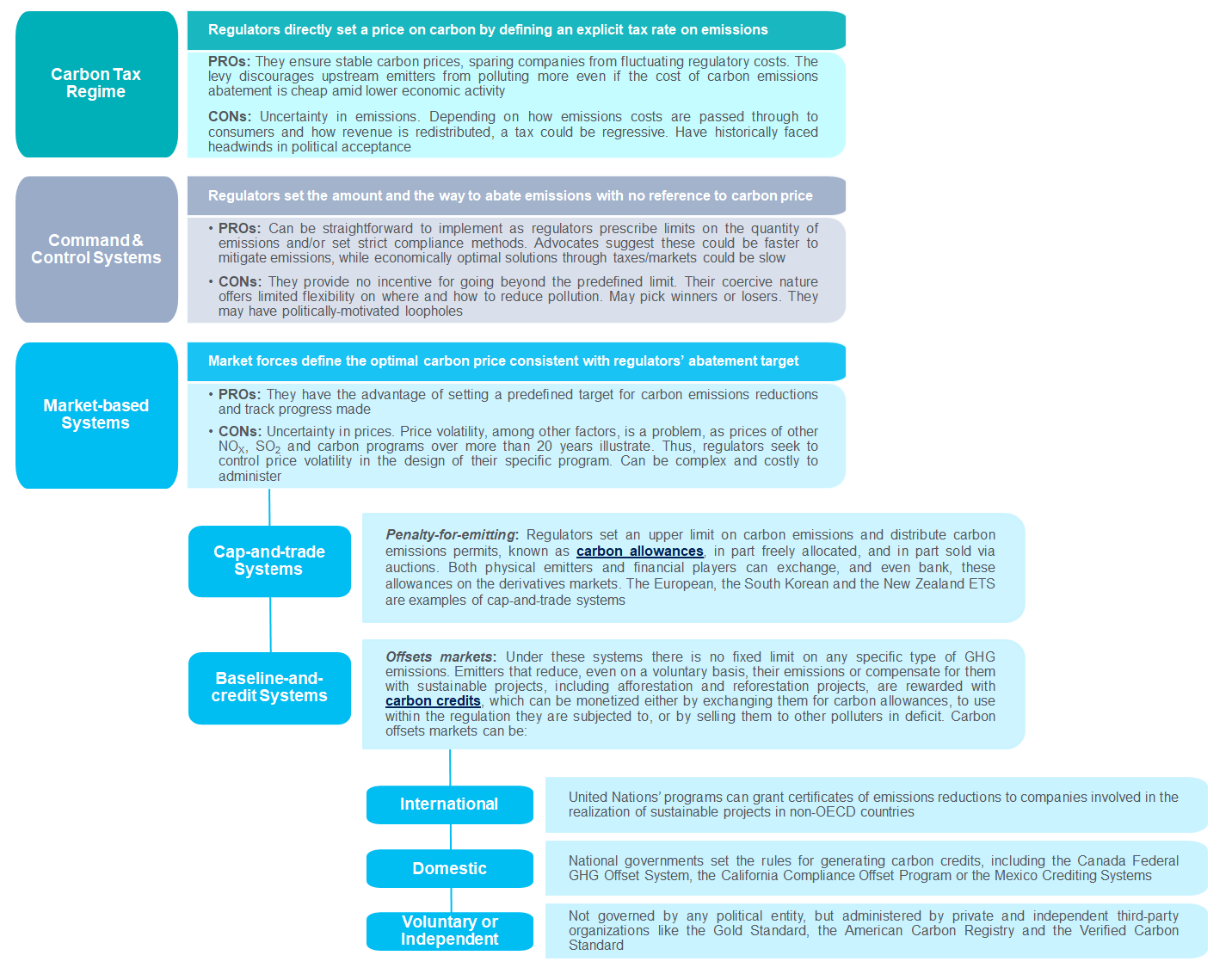

A framework for emissions pricing |

|---|

|

Source: Citi Research |

The basics

Carbon crediting is the process of issuing tradeable securities to projects ensuring sequestered or avoided greenhouse gas emissions. Each carbon credit awarded to the developer of such a project represents one ton of carbon dioxide emissions or its equivalent in other greenhouse gas emissions, including potentially methane, nitrous oxide, perfluorocarbons, hydrofluorocarbons and sulfur hexafluoride, whose occurrence must be verified by an international, domestic, or independent registry.

Generally, eligible projects could belong to any of the following categories:

|

The vintage year of a carbon credit refers the year in which its associated emissions reduction effectively occurs, although for some projects the registry could issue the carbon credits on the basis of the reporting year; there could be a significant time lag between the two periods. Once issued, these securities can later be either surrendered by the same developer within the compliance carbon market it is subjected to – if any – or monetized in the secondary market to other buyers. These buyers are typically other emitters, which may have to comply with or are voluntarily implementing emissions reductions activities.

There are also brokers, such as financial institutions, that could facilitate the transaction, but could be also willing to purchase the carbon credits to bank them on their own balance sheet and resell them later. Once a carbon credit has been retired or outright cancelled, meaning it has been removed from its own registry, it has served its climate purpose and can no longer be resold. For more information on this subject, please see Global Commodities - COP26 and nature-based solutions catalysts for growth of carbon credit markets

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.