Recession risks are top of mind for both markets and corporates and recessionary dynamics are increasingly present. Citi economists’ view is that there is a 50% chance of a global recession, but that it’s more likely to happen in 2023.

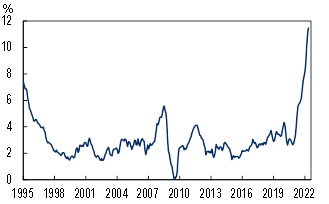

Global Headline CPI Inflation |

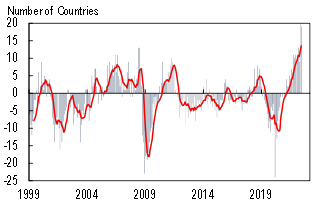

Tightening in Global Central Bank Policy (Net)* |

|

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, National Statistical Sources, Haver Analytics |

*Across 33 central banks, the number hiking (+) or cutting (-) the policy rate each month. Red line denotes 6-month moving average. |

|

Source: Citi Research, National Statistical Sources, Haver Analytics |

Here’s a summary of current thinking:

- Citi economists now see contractions over the next 12-18 months in the Euro area, the United Kingdom, and—towards the end of the period—the United States.

- In the EM world, they see recession in Brazil, Chile, Hungary, and Turkey, in addition to the sharp ongoing contraction in Russia.

- The timing of these recessions is expected to vary, based on each economy’s exposure to global shocks and its underlying momentum.

- For example, economists see the Euro Area contracting in Q4:22 and Q1:23, as high natural gas prices and lagging real wages take a bite out of consumer spending.

- The U.S. economy, in contrast, is continuing to show more momentum, especially in the labour market and services spending, and Citi economists are not expecting recession until the second half of next year, as the cumulative effects of Fed rate hikes eventually halt the expansion. In general, these downturns are expected to be relatively mild.

- The underlying drivers of performance across countries are broadly similar. Surging inflation pressures are afoot, with global headline inflation running at its hottest pace in decades. These pressures have led central banks to launch a tightening campaign that is the most concentrated in more than 20 years.

- As a closely related matter, global economic activity continues to be constrained by challenges from the pandemic, including the risk of new variants and renewed lockdowns (especially in China), as well as stresses from the Russia-Ukraine war.

Global Growth Forecasts |

Global Inflation Forecasts |

|

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research |

Source: Citi Research |

- One intensifying downside risk for both Europe and the global economy involves the reliability of Russian gas supply.

- For China, with the economy coming out of lockdowns, the data are showing mounting evidence of recovery. In addition, the government looks to be in the process of implementing stimulus measures, which should set the stage for stronger subsequent growth.

By any metric, the global economy is slowing—and prospects are deteriorating. But two factors help keep aggregate global growth in positive territory. First, the projected recessions are relatively mild and, second, their timing varies.

For more information on this subject, please see Global Economic Outlook & Strategy: Global Recession—A Clear and Present Danger

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.