The pandemic’s ripple effects are likely to continue for years to come, although the simplistic winner/loser rubric should no longer suffice, with each sub-sector within leisure, and for that matter each company, carrying very specific investment dynamics.

For all those variations, Citi Research has identified five important themes in leisure that it thinks could shape the industry as it remerges from the pandemic.

THEME 1: Enduring Nature of the Outdoor Demand Surge

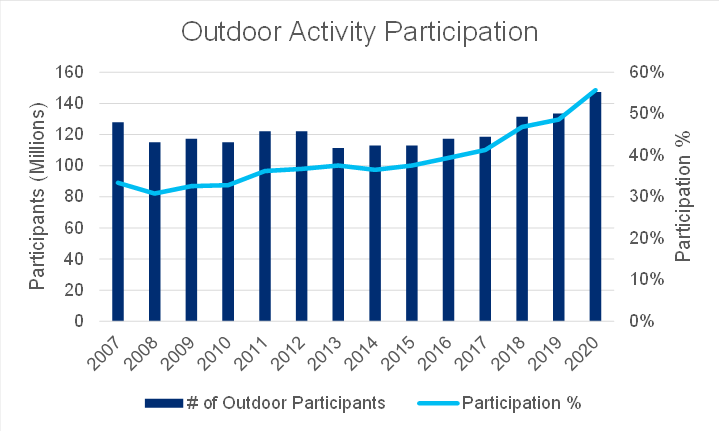

The 2020 reopening came with strings attached, with entire categories of leisure and travel activities off the table. Consumers flocked to outdoor activities in record numbers.

While leisure purchases have been much more influenced by product availability, outdoor participation trends have been universally positive.

|

Outdoor Activity Participation Over the Years |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, Outdoor Industry Association |

Anecdotally, growth has disproportionally come from those new to the activity.

During the onset of the pandemic, the entirety of leisure was hit hard, with stay-at-home orders, travel restrictions, and dealer closures combining to decimate demand starting in late March 2020. However, in a fairly shocking (at the time) turn of events, powersports companies were among the earliest beneficiaries of reopening as consumers quickly flocked to these products as soon as dealerships reopened and, in some instances, even before. In the ~22 months since, the outdoor surge has been unprecedented, with demand in a number of powersports categories (namely side-by-sides, boats, and RVs) reaching record levels and others (motorcycles, ATVs) seeing sharp resurgence and substantially besting 2019 levels.

Looking forward, Citi Research expects the surge in demand for the RV lifestyle to be the most sustainable, as this was already an area with significant secular and demographic tailwinds that shifted into higher gear during the pandemic. Long before COVID, the RV industry experienced its most prosperous period on record during the eight years following the Great Recession. As an aging Baby Boomer generation has created sizable headwinds for powersports products across the spectrum, within the RV space, an increasing number of retiring boomers and a burgeoning millennial generation are creating a demographic tailwind unlike any in the industry’s history.

THEME II: Late-Stage Reopening – How Much Pent-up Demand Remains?

The cruise industry was hit as hard as any in the early days of the pandemic, incurring negative press and, in several instances, being shunned/stranded offshore.

Citi Research notes an overarching belief by some that cruise demand is permanently impaired among a significant portion of the population. It reckons that certain potential passengers will be harder to convince to return, but a long history of destabilizing events suggests that even these customers eventually will.

Citi Research also expects an abundance of customers who are more than willing to re-engage cruise travel and who will be looking to make up for lost time. When all is said and done, more than 50 million passengers will have missed out on a cruise vacation over the course of the pandemic, a massive number for an industry that typically carries 33 million passengers per year—many of whom are consistent repeat passengers.

THEME III: Supply Chain/Cost Inflation/Product Availability

Supply-chain issues have been ongoing since the start of the pandemic, but the cause has evolved over that time. In the early going, lockdowns and health and safety measures limited the operations of nearly every industry, manufacturing facility, and port in the world. As vaccinations have progressed and the world has reopened, this has been replaced with red-hot demand far exceeding the usual volume of the existing production and shipping infrastructure.

Throughout various points in the pandemic, supply chains have suffered from delays, COVID-related headwinds, various parts and materials shortages/backlogs, and rapidly rising shipping costs. The ongoing headwinds affecting supply chains are unlikely to be fully resolved or fully abate any time soon—pushing restock cycles further out while compressing gross margins.

On the cost side, the most widely used raw materials among the manufacturers are metals (such as aluminum, steel, and copper and petroleum-based resins), all of which are up year over year and are up much more so over pre-pandemic levels but are down versus their summer/fall 2021 highs.

Adding to this, however, are ongoing inflation in transportation and logistics costs, including hefty sums required to expedite components as well as finished goods, which most leisure companies have been more than willing to do in an effort to maximize product availability.

THEME IV: Labor Availability/Wage Rate Inflation

In the same way that manufacturers had supply-chain issues during 2021 (not only eating into margins but also limiting their ability to deliver product to consumers), theme park companies were impacted by both labor availability and significant wage rate inflation.

Theme parks have been dealing with rising wages for most of the past five years, in large part due to local minimum wage increases, as the majority of positions at parks target minimum-wage workers.

The after-effects of COVID shifted this issue into high gear during 2021, however. Given a sizable backlog of visa applications, long processing times, logistical challenges, and health risks brought on by COVID-19 for would-be guest workers, several theme parks have been hampered by a lack of international workers, which have historically accounted for a large component of some parks’ seasonal workforces.

THEME V: Unprecedented Pricing Power Showing No Signs of Abating

Few dynamics have ever cut across leisure coverage like the robust pricing power that we saw during much of 2021 and that is showing no signs of abating at the start of 2022. The manifestation of this pricing power is different within each of the verticals, and yet the effect is largely the same. Citi Research expects that the magnitude and duration of pricing and promotional strength will comfortably outweigh the headwinds associated with the supply-chain hiccups/raw material inflation and wage rate inflation, at least in most cases, with the net benefit only growing over the course of 2022.

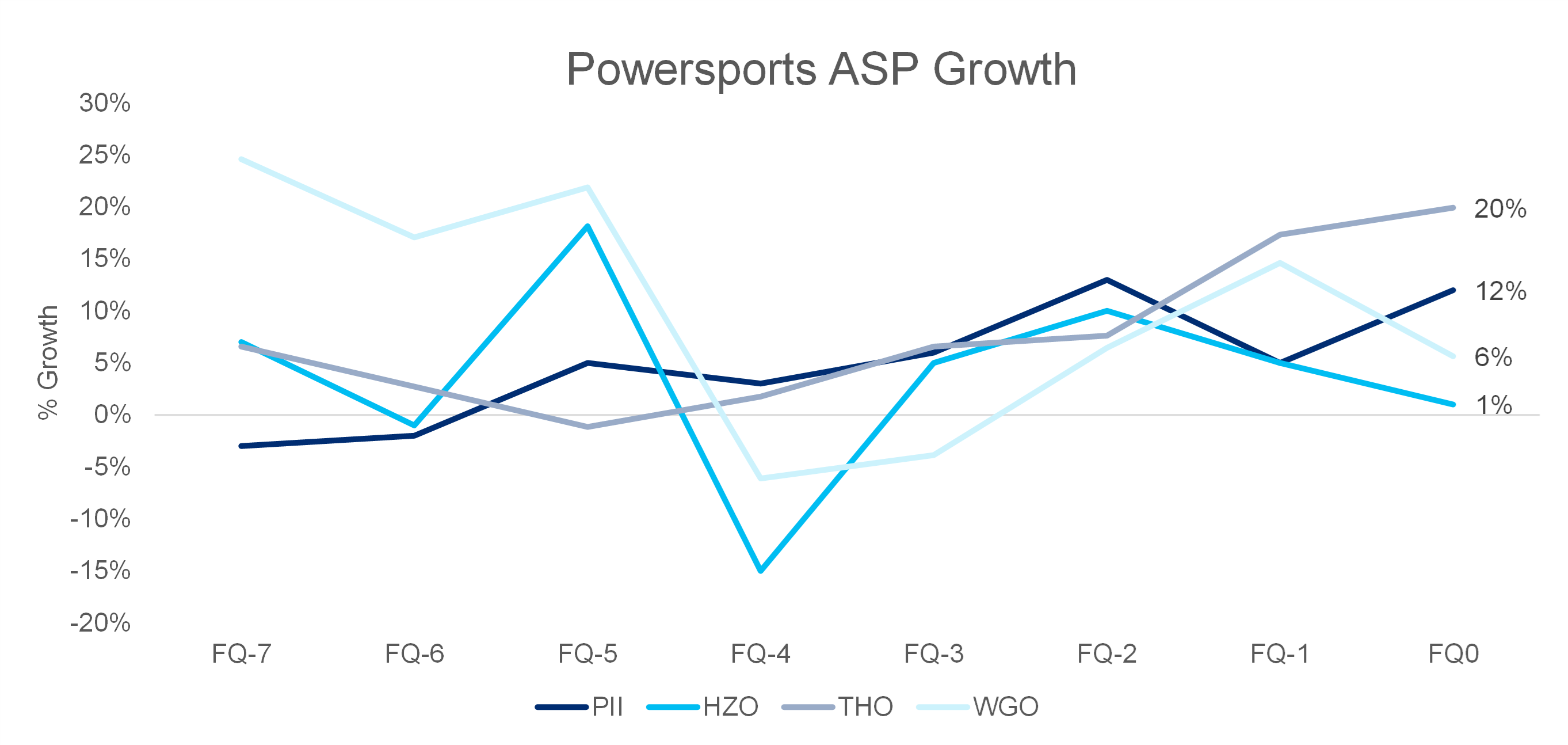

In the powersports/RV space, which has historically been one where promotions, discounts, and rebates have played a pivotal role, there has been little need to provide any of the above. This has particularly been the case as inventories have waned and availability has dried up in the dealer channel, leaving consumers little choice but to pay full price.

ASP Growth Among Powersports Companies |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research, Company Reports |

Additionally, as raw material inflation has become an increasingly high-profile issue, powersports manufacturers have raised prices to offset this inflation. Different manufacturers and different products have taken different routes to price increases, including price-to-cost, price-to-market, model-year price increases, mid-model-year increases, and surcharges. The different strategies point to different assumptions about the elasticity of demand, the availability of product, and the future ability to maintain (or extend) price increases even assuming that material inflation wanes.

The full report goes on to look at a number of macro and micro trends affecting the leisure sector and the outlook in 2022 for a space that was dominated by COVID and supply chain factors during 2020 and 2021. For more information on this subject, please see US Leisure - The ‘Outdoor Renaissance’ and the Return of Alpha to the Leisure Sector.

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.