Nuclear power currently represents 3% of global energy investment. But Citi analysts reckon nuclear energy has the potential to double its share amid shifting geopolitical factors. Europe is pivotal to any substantive re-think of the role of nuclear power.

Citi commissioned a survey of 10,000 European residents and concluded that two-thirds would now support a new nuclear policy – that’s up 25% since the Russia-Ukraine conflict (survey was conducted three weeks after the conflict began). Signs of changing sentiment are also apparent in South Korea.

Nuclear energy’s low-point, at least in many developed economies, was post Fukishima in 2011. The accident created a backdrop of anemic new investment and commitments to close capacity in several countries.

However, rising and volatile electricity prices – even before the Russia-Ukraine conflict – have seen policy-makers starting to question what power systems look like under deep renewables penetration. Citi analysts say they believe nuclear energy can fill a necessary (and low carbon) role in balancing the grid.

Key finding of survey: While the full Citi report is global in its reach, much of the focus is on Europe because that region is regarded as offering the greatest scope for change. Although the Citi analysts say the impetus was already there, the Russia-Ukraine conflict appears to have acted as a catalyst for the European public’s greater endorsement of new nuclear power efforts.

Opportunity/size — Citi analysts estimate the potential need for over $500bn of investment in new nuclear just for Europe, South Korea and the US over the coming two decades. Adding in existing markets such as China and India, as well as likely investment in plant extensions, that adds up to an estimate that nuclear power could be an $80 billion/year industry by 2030. This would take nuclear from around 3% of global energy spend today to a little under 4% by end-decade, a substantial increase but still relatively niche versus the spending expected into renewables and the transmission networks.

A nuclear thaw

Given the current geopolitical backdrop, European politicians are facing the challenge of rewriting the region's energy policy. Reducing high dependence on Russian energy is one obvious outcome, a topic Citi addressed in Europe/Russia: Where Can Energy Capital Flex?

Cracks in European energy policy were beginning to appear before the Russia-Ukraine conflict. Several factors led up to this – including rising electricity and gas prices in 2021 – but one major cause was the low output from wind during the summer months. The question to be addressed is: How should Europe manage an energy system that faces a rising risk of intermittency?

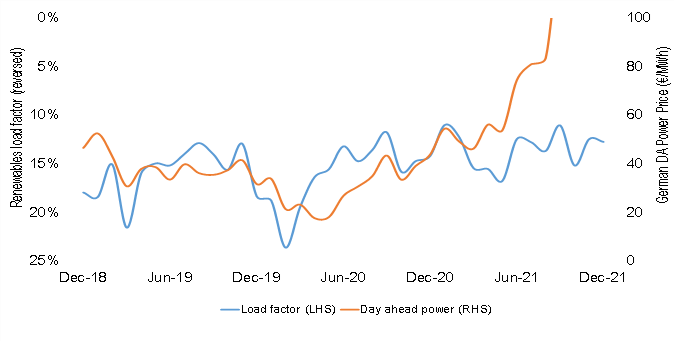

Renewable Penetration Has Led To Increased Power Price Volatility |

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: www.smard.de, Citi Research |

Europe’s long-term policy pathway – e.g. 'Fit for 55' – seems to be to overbuild renewables and with excess power towards green hydrogen as a long-duration storage mechanism. In Citi’s view, this policy makes little sense on the point: who would build renewables capacity if power prices were too low? Yes, green hydrogen costs appear to be coming down, but fundamentally the economics of electrolysis rely on the unsustainable proposition of zero or negative electricity prices.

So rather than risk everything on a Plan A policy, Citi analysts say Europe might now look to Plan B or at least a Plan A*. This new plan would place greater value on having capacity in baseload power generation and storage. This could be based on fossil gas, for which plants are quick to build and have relatively low upfront capital, but these emit carbon and bring in the Russia-dependency issue. As such, Europe will likely have to embrace a larger role for nuclear power than might have been envisioned otherwise.

After extensive lobbying, the EU investment taxonomy proposal envisages support for investment in both fossil gas and nuclear. Any pivot to nuclear power would require public support and for that reason would likely be focused in a small number of countries (France, UK, Poland, and potentially Belgium), while Germany may be reluctant to re-visit its decision to shut down nuclear power.

Citi’s survey, conducted with its Innovation Lab unit, was of 10,000 voting-age adults, representing general population by age and gender across seven countries (Belgium, France, Germany, Italy, Poland, Spain and the UK).

Respondents Have Become More In Favour Of Nuclear Power Since The Conflict

|

|

|

|

© 2022 Citigroup Inc. No redistribution without Citigroup’s written permission. |

|

Source: Citi Research |

Several cuts of the data are shown in the full report, but the real standout highlighted by the Citi analysts – and illustrated in the chart above – is that across Europe the conflict has triggered a dramatic change in how people think about nuclear power.

Some other key survey results |

|

|

While power generation from renewable sources brings with it all the benefits of zero emissions, it also introduces a degree of volatility, being tied to weather patterns – when the sun shines, the wind blows or the rain falls. This impacts both power prices and system balancing costs.

Across the globe, 439 nuclear reactors are currently in operation, totaling 393GW or around 11% of global power generation capacity. Europe (EU 27 + UK) holds around one third of total capacity; US and China combined are around 40%. Of 56 nuclear reactors under construction, only five are in Europe.

Citi’s analysis implies the need for new-build nuclear capacity to maintain its current role in Europe’s power systems. Until recently at least, that was not the direction of travel from policymakers. Whether influenced by Fukishima in 2011 or by concerns over costs, EU policy either has been non-committal or negative. The Russia-Ukraine conflict may have significantly shifted that sentiment. Find the full report, first published on April 11th here Global Power - Changing Sentiment May Allow Nuclear Power to Scale

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.