The semiconductor industry is the driving force behind such technological innovations as artificial intelligence, electric vehicles, and factory automation, playing a crucial role in nations’ economic prosperity and national security. Despite accounting for 25% of total semiconductor demand, the U.S.’s total semiconductor manufacturing capacity is just 12%, down from 37% in the 1990s. That has sparked concerns about a threat to national security given China’s efforts to gain a significant foothold in this vital industry.

Source: Citi Research, TechInsights, SIA, and Gartner

A key focus of the report is the CHIPS and Science Act, which became U.S. law in 2022. Its aim is to boost domestic chip production, with $52.7 billion earmarked for allocation over five years to develop domestic manufacturing, as well as R&D and workforce programs.

As part of the CHIPS Act, semiconductor companies will get 25% investment tax credits for investing in semiconductor manufacturing or specialized tooling equipment. But as the report notes, the CHIPS Act faces challenges in turning its goals into realities. In March, the Commerce Department introduced conditions for companies seeking $150 million or more in funding, including stock buyback limitations, profit sharing, and a preference for union labor. The report warns such conditions could make returning leading-edge semiconductor manufacturing to the U.S. extremely difficult, with companies working to stay below the $150 million threshold.

The former chair and CEO of the Taiwan Semiconductor Manufacturing Company (TSMC), a behemoth that produces 90% of the world’s most advanced processor chips, estimates that it would cost up to 50% more to make leading-edge chips in the U.S. than in Taiwan due to labor costs and different worker norms.

And most semiconductor companies don’t need extra funding, as the industry is one of the world’s most profitable. That leads the authors to conclude that only less-profitable chip companies may prove more willing to participate in the CHIPS Act in its current form, limiting its industry impact.

Semiconductor companies that choose to manufacture chips in-house are known as Integrated Device Manufacturers (IDMs), with the plants that make such chips called fabs. Another model for the industry is to go “fabless,” outsourcing the manufacturing process to a foundry. And some companies have chosen a hybrid model.

The Semiconductor Industry Association estimates that the 10-year cost of a state-of-the-art fab ranges between $10 billion and $40 billion, up from less than $1 billion in 1997. Only four IDMs—Samsung, Intel, Hynix, and Micron—have the scale necessary to support construction of leading-edge fabs. Other semiconductor companies, including Nvidia, AMD, Qualcomm, and Marvel, have outsourced some or all of their manufacturing to TSMC.

Source: Citi Research, TechInsights, SIA, and Gartner

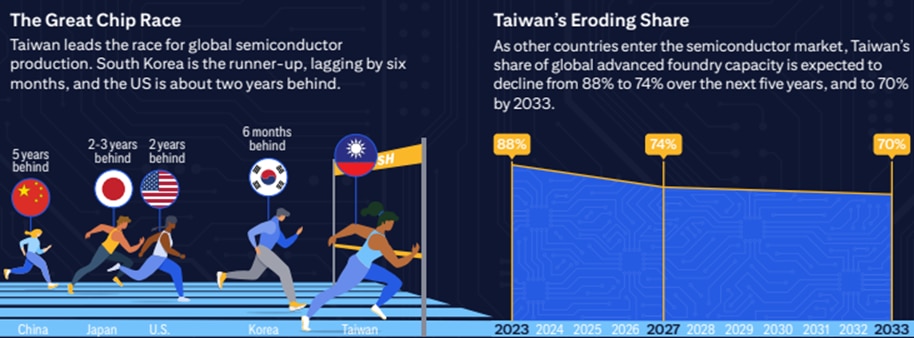

TSMC is the clear leader among the five major foundry companies, with a 58% share of the global market. In 2021, Intel announced it would refocus on the foundry business with an eye on overtaking Samsung as the second-largest foundry by 2025. But the authors point to several obstacles that got in the way of Intel’s ambitions—including rigid design rules and talent churn, and the fact that the foundry business model is totally different than that governing Intel’s CPU business.

Meanwhile, TSMC is rushing to establish fabs outside Taiwan as a hedge against supply chain disruptions that might arise from the region’s geopolitical tensions. The authors think this move will help TSMC hold onto most of the foundry business, although they note it has been having trouble establishing a leading-edge foundry in the United States. Samsung’s foundry business, on the other hand, is expected to benefit from the CHIPS Act given its 27 years of foundry experience in the United States.

The CHIPS Act isn’t the only tactic deployed in the U.S.–China chips rivalry. The U.S. and its allies are also using sanctions on China. These date to 2017 and U.S. action against ZTE; in October the U.S. Commerce Department’s Bureau of Industry and Security further tightened export controls on advanced semiconductor production equipment and high-performance computing chips. Such restrictions have limited China’s ability to acquire and make advanced chips, with an emphasis on items or technologies used for supercomputing and AI training. The export restrictions also apply to non-U.S. vendors and exporters, which has led Japan and the Netherlands to limit their semiconductor-making technologies. The authors note their belief that China’s advanced semiconductor fabs are still capable of producing chips in limited volumes, which will likely lead to further sanctions.

The European Union has created its own take on the CHIPS Act with the European Chips Act (ECA). As with the U.S., only about 10% of global chip manufacturing is situated in Europe; the EU aims to double that to 20% by 2030. European and international chip makers have already committed to R&D and fab expansion plans in Europe in hopes of accessing funding from the ECA and other sources. Because the ECA lacks the restrictions that come with the CHIPS Act, chip manufacturers seem to have few if any reservations about accessing this funding.

Japan has pursued its own drive to establish semiconductor production facilities, with 2022’s Economic Security Promotion Act outlining a framework for combined public and private financing of ¥10 trillion over 10 years. Japan accounts for 12% of global semiconductor consumption, but its share of production capacity is extremely low. Semiconductor industry activity is booming in Japan, a development that has been fueled by expectations for growing demand for Japanese-made chips as sourcing diversifies out of Taiwan. Japan has been encouraging foreign companies and foreign capital to play an active role, with examples of entities pursuing investment and collaboration including TSMC subsidiaries, Taiwan-based PSMC, and U.S.-based Micron.

A redacted public version of the report, first published on 30 November 2023 and including a Q&A with semiconductors expert Chris Miller and a graphical overview of the semiconductor industry, is available here.

Citi Global Insights (CGI) is Citi’s premier non-independent thought leadership curation. It is not investment research; however, it may contain thematic content previously expressed in an Independent Research report. For the full CGI disclosure, click here.