My Account

Securities Services Evolution 2023

Disruption and transformation in financial markets infrastructures

Securities Services Evolution 2023 tracks the continuing evolution of our industry from being on the brink of change (in 2021), to seeing ongoing transformation (in 2022), to a year in which execution and realization have become core priorities in 2023. Not only is the industry preparing to remove an entire day from the settlement cycles of the world’s largest capital market, but firms are also readying themselves for what they expect to be imminent changes to other settlement cycles, digital currency adoption and even atomic settlement in the next five years.

The central theme of this year’s whitepaper revolves around the volume and diversity of change that market participants are facing around the world. This change centers on three broad areas:

FMI transformation: Significant change pressures being felt by financial market infrastructures across the world to manage a growth agenda during a phase of major technological transition (and removal of legacy platforms).

Settlement transformation: Preparations by all profiles of global market participants for accelerated settlements in the US and Canada (transitioning in May 2024) and more to follow — giving rise to a new, real-time target operating model.

Digital assets and DLT: Adoption and live deployment of digital assets (including crypto-currencies) as well as tokenization projects (digitizing traditional securities), building on the increased optionality that DLT offers each firm.

The FMI agenda

Across the world, FMIs (most notably the Central Securities Depositories, or CSDs) are almost all facing the same two headline challenges: How to accelerate ransformation and innovation (in settlements and digital assets above all) while at the same time managing a transition away from ageing, legacy infrastructures. Across digitization, accelerated settlements and legacy transition, the ecosystem impacts of these pressures are now top-of-mind for many FMIs, as they shift their historical focus from managing (their own) platforms towards managing a wider ecosystem. From owning individual change to facilitating change across the industry.

While FMIs struggle with these challenges almost uniformly, almost regardless of location, there are important differences. In Latin America, we are about to see one of the most ambitious consolidation projects ever realized between Colombia, Peru and Chile. In Europe, the lasting benefits of clearing competition are now coming into question. In the digitization space, those in Asia and Latin America continue to innovate to drive financial market participation — while their peers in North America and Europe are shifting their focus towards the provision of common industry platforms. In Europe, Australia and other markets, corporate action standards continue to be a focus.

Faced with what seems to be an inevitable acceleration in settlement cycles (coming to the US, Canada and most likely Mexico in 2024), FMIs look set to have an increasingly complex operating agenda for years to come.

Settlement transformation

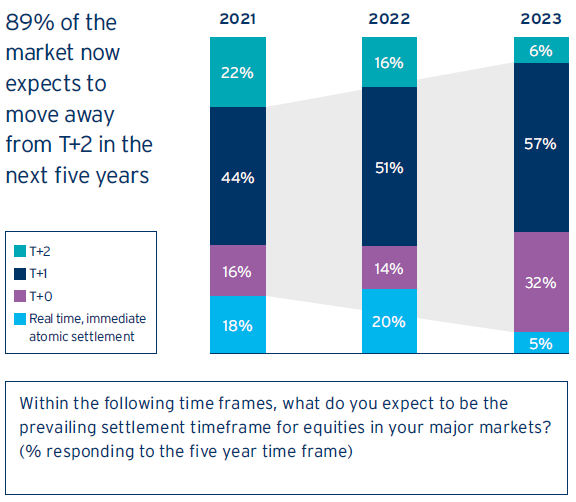

89% of our survey respondents expect their local settlement cycles to shorten to T+0 or T+1 within the next five years. This means a vast amount of change ahead for an extended period. As firms across the world are discovering with their preparations to T+1 settlement cycles in the US and Canada next year, the impacts of accelerated settlement are profound and touch everything from trade fails to headcounts and treasury requirements. Next year’s transition will impact up to eight different departments in each organization but in differing ways, depending most of all on where firms are located in the world. Those in Europe and Asia will be profoundly impacted by the treasury implications of T+1, while those in North America contend with regulatory requirements and securities lending liquidity.

With each market transition, the industry’s best-practice sharpens a little. After India’s T+1 move in early 2023, the path towards market readiness is clear: First get clients and counterparties engaged; then drive internal automation; and finally put in place resources and location strategies. Across all of these areas, the ability to depend on real-time communications, feeding a realtime view of inventory is increasingly critical.

With each market move increasing dislocation risks between different global settlement cycles, the likelihood of the T+1 domino effect continuing is high.

DLT and digital assets

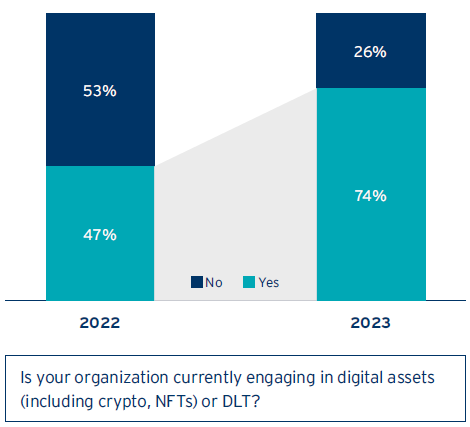

2023 sees 74% of our respondents engaging in distributed ledger technology (DLT) and digital asset initiatives (increased from 47% in 2022), in a clear sign that the DLT momentum continues to grow, despite negative news headlines around FTX and other initiatives. But while digital asset and crypto-currency activity continues (notably in Europe and Asia), building and preparation activity seems increasingly focused on DLT and tokenization, as the industry looks to leverage the choice and flexibility that the technology offers in operating processes and market rules.

As this increased activity moves into live environments, the dependencies that lie ahead are becoming more granular. In need of a currency leg for digitized transactions, the industry is increasingly bullish on their expectations of digital cash being operational within five years (through a range of Central Bank Digital Currencies (CBDCs) and more commercial mechanisms).1 Organizationally, the focus is increasingly on those whose role it is to govern our infrastructures — not just regulators but also risk, compliance and finance teams. Technologically, there has also been a marked shift in who is expected to manage the burden of legacy platform connectivity — from the market participant to the provider. And lastly, but not least importantly, financial markets regulators across the globe are sharpening their guidelines and legislations to ensure continued oversight on market integrity and investor protection.

Looking ahead, the continued momentum of DLT and digital assets looks set to depend on two factors. First is the sell-side’s ability to successfully engage the buyside, using a narrative that is built around the needs of a portfolio manager (more than an operations head today). Second is the ability to change industry processes to realize the benefits that DLT offers.

Related Stories

Securities Services

Get in Touch