There’s a lot of buzz these days around real-time liquidity. That’s because, despite being in a nascent stage, the long-sought-after ability to manage liquidity in real-time is on a course to becoming a reality very quickly. For treasurers this means staying on top of everevolving marketplace and technology developments and taking the incremental steps necessary to keep their organizations on a sound path to reaping the many benefits of viewing and mobilizing funds in real-time. Treasuries that fall behind will find it difficult to support new e-commerce models and “just-in-time” supply chains, which can help reduce commercial counterparty risks and enhance working capital.

Rupa Mankad,

APAC Head of Liquidity Solutions Product, Treasury and Trade Solutions, Citi

Ambrish Bansal,

Global Head of Liquidity Solutions Product, Treasury and Trade Solutions, Citi

Fueled by instant payments

The forces propelling the shift to real-time are numerous. One of the most significant is instant payments. Instant Payments schemes have been emerging rapidly over the past few years. Today there are more than 55 live Instant Payments schemes globally, covering 85% of the world’s GDP. Payment networks that enable the transfer of funds from one bank account to another in a matter of seconds are being rolled out in local markets around the world in growing numbers — with the expectation that most key markets will have a live Instant Payments scheme by 2023 — redefining payment preferences and reshaping cash flow management for both buyers and sellers.

In Asia, regulators were at the forefront of launching instant payment schemes, moving a commercial culture immersed in digital payments and mobile banking to new levels of speed and efficiency. With instant payment networks now live in over 13 markets in Asia Pacific1, major markets such as South Korea, India and China see daily instant payment flows of roughly 75 million, 41 million and 30 million, respectively.2

Globally at Citi, an estimated 1.8MM of instant payment transactions are processed daily and schemes are now live in 27 countries, including all major markets, with an additional 10 markets expected to go live by year end.

This intensification of growth points to the widespread adoption of e-commerce channels among digital natives and traditional businesses, as well as their desire to meet the expectations of digitally savvy consumers.

A matter of supply and demand

By their nature instant payments play a key role in the march toward real-time liquidity. More broadly speaking though, the speed and essence of the shift to real-time liquidity is intricately linked to the fundamental economic forces of supply and demand.

Demand is being driven by the proliferation of e-business models, marketplaces and platforms, including a rise in direct-to-consumer e-commerce, all of which picked up unprecedented momentum during the Covid-19 pandemic and are fueling the appeal of real-time transactions.

On the supply side, technical and market infrastructures have also evolved rapidly in recent years. Part of this evolution is tied to the surge in instant payment schemes that enable banks and fintechs to mobilize funds in real time. On a wider scale, however, open banking and application programming interfaces (APIs) are two of real-time’s most powerful enablers, particularly when it comes to the messaging layer of transactions and the exchange of data among banks and other ecosystem participants.

As for open banking, one of the most widely known regulatory initiatives aimed at opening up data flows between financial institutions and third parties via APIs is Payment Services Directive 2 (PSD2) in the UK and EEA. However, numerous other markets are on a similar path. Australia and Hong Kong, for instance, have established open banking frameworks, and in the U.S. the Consumer Financial Protection Bureau (CFPB) has proposed open banking rules around the exchange of consumers’ transaction data. While markets like China, India and Thailand don’t have formal regulatory guidelines the off-take driven by the commercial uses and emerging from the underlying digital economy is sizeable.

As instant payments take off in markets where there are no regulatory-prescribed limits, such as Hong Kong and Australia, instant payments are gaining traction in the B2B environment too.

Bottom line, rapidly changing forces on both the supply and demand sides of the equation are driving real-time operating flows and making the time very ripe for the development of real-time liquidity.

Plotting a path forward

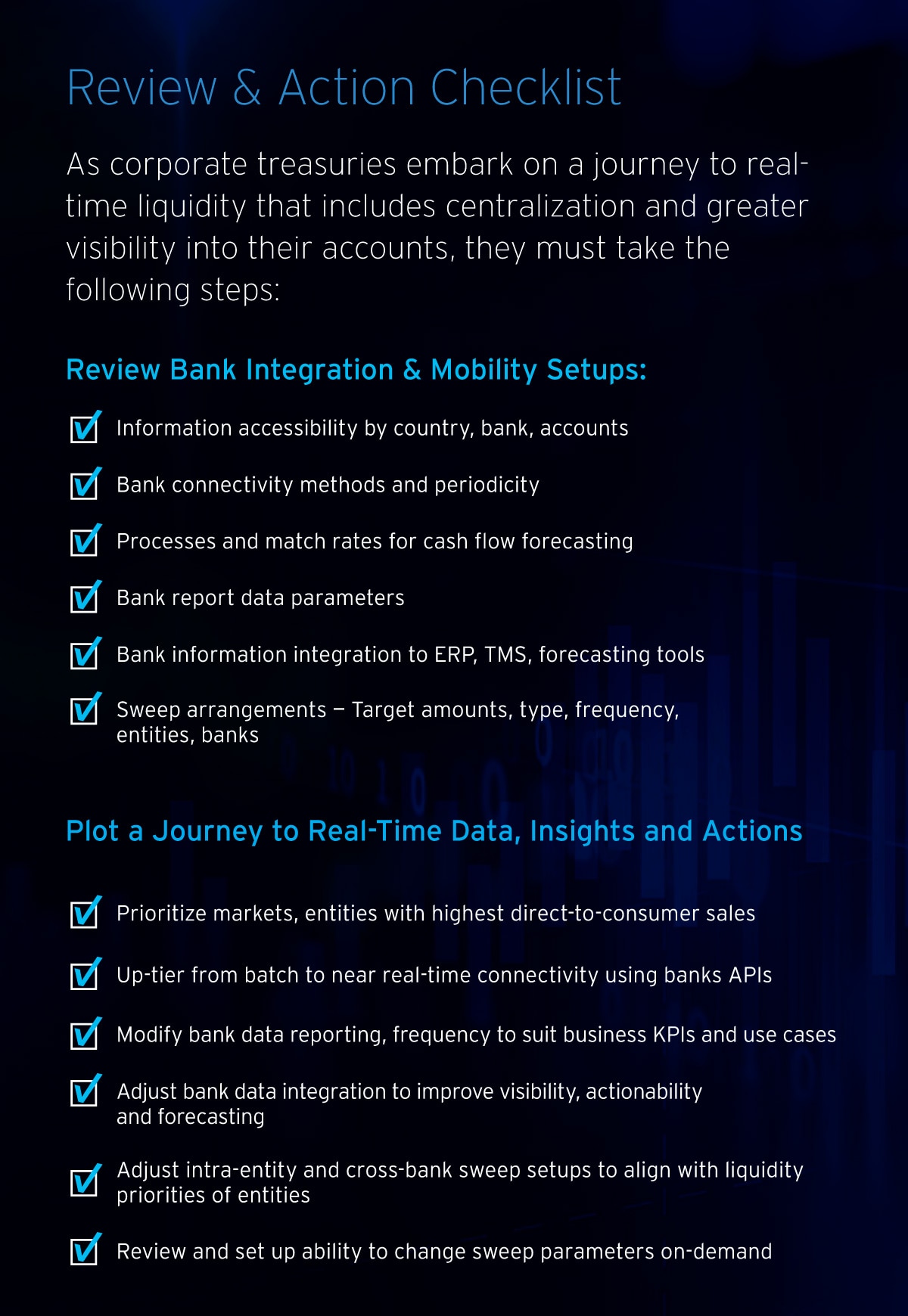

When it comes to plotting a course to achieving real-time liquidity, one size does not fit all. All organizations face challenges that are unique to them determined by a wide range of factors such as industry sector, organizational structure, geographic footprint and technology readiness.

Generally speaking, though, a company’s multi-year journey to real-time liquidity will parallel marketplace developments and encompass several phases. In all cases, however, the process starts with taking stock of treasury’s current state and clearly defining the problem or problems to be solved. First steps in the journey also include putting in place the right team to properly scope the work to be done, secure the requisite funding, and get the job done with technology support from the highest levels of the corporation being essential.

Organizations that homogenize Enterprise Resource Planning (ERP) and achieve some level of visibility into accounts across multiple banks are best suited to graduating toward real time. Establishing a high degree of digitization and centralization ensures that a company is well positioned to take the next step: leveraging Application Program Interface (API) to access balance information and other actionable data faster, even in real-time or near realtime in certain markets.

Educating internal business partners and senior business managers is also a key step in any transition. Unless there is perfect harmony between what treasury can bring to the table and where business partners are headed and see value, the adoption of real-time liquidity and cash management will be stalled.

Organisations gradually mature from real-time cash pooling across entities, currencies to multibank cash pooling solutions as the market infrastructure evolves.

As the global infrastructure on inter-operability of instant payments and regulatory support on 24*7 liquidity evolves further the bank supported real-time and 24*7 liquidity solutions will also evolve and will be made available in a more harmonized fashion.

Enhancing treasury processes

The significance of APIs in making real-time liquidity a reality is colossal. APIs, which function as the connective tissue that enables disparate technology platforms to talk to each other, are the linchpin in two primary components of liquidity: visibility and mobility, both interbank and intrabank.

As open banking initiatives take hold, banks are increasingly employing APIs to exchange data in their systems, such as account balances, with each other, which in turn enables them to offer their clients services such as multibank target balancing and reporting, for instance.

Equally important, however, is how banks are deploying APIs to open up back-end data functions to their clients, exchanging transaction and account data directly, and immediately, with treasury workstations and other enterprise platforms.

In fact, banks are continuously leveraging next generation technology and infrastructure advances such as SWIFT gpi to introduce new tools and capabilities that set new standards for speed and efficiency while laying the requisite groundwork for ubiquitous real-time liquidity management.

Citi, for example, now provides clients not only with real-time visibility of their balances in the accounts with Citi but goes further by providing the ability to make modifications to their pooling structures3 on their own in minutes, making it easier to respond quickly to changes in business models or cash flow forecasts. Users of the CitiDirect BE® Cash Concentration portal can perform a wide range of adjustments to their structures themselves, including modifying target balancing parameters, suspending or reactivating sweep pairs and amending interest reallocation rates, to name a few. This marks a strategic shift toward on-demand liquidity management especially for industries whose cash-flows have a very large share of direct to consumer flows and thereby near-real-time cash flow use-cases.

Citi also offers a real-time liquidity sharing capability that automates and optimizes the use of net available balances dispersed across multiple entities, and accounts. It enables real-time intraday sharing of liquidity i.e. virtual lending and borrowing between pool accounts via a single global platform with automated liquidity controls and limits management. This intra-day liquidity sharing is accompanied with an end-of-day settlement of obligations between pooled entities, thereby supporting frictionless real-time payment intra-day and at the same time minimizing co-mingling of funds across entities.

Such offerings reflect Citi’s commitment to developing solutions that make liquidity management more resilient to the ebbs and flows of incoming and outgoing payments, on an intraday basis, and ensuring that zero balance accounts and liquidity pools actually support frictionless payment flows, irrespective of where funding is available within a pool.

While many solutions at Citi are developed in-house, it also partners with strategic fintechs and software firms to integrate its capabilities into their platforms and create new turnkey solutions. And it co-creates solutions with clients interested in being on the bleeding edge of new treasury management opportunities.

Tapping banking partners

No matter where a company is on its liquidity optimization curve, it is wise to discuss goals, objectives and opportunities with banking partners. They can provide guidance and assistance on the best ways to support new business models, get the technology right — for today and into the future, and also how to leverage existing technology to take cash and liquidity management to the next level.

On a constantly changing technical and marketplace landscape, a capability that is not available today may be on the near-term horizon. Top providers like Citi can help treasuries stay on top of emerging trends and are constantly rolling out new capabilities that help optimize liquidity, maximize returns and advance real-time objectives.

To learn more about preparing for and pursuing a path to real-time liquidity, click here to hear experts from UPS and Citi share real-world insights and best practices at Citi’s 2021 Corporate Liquidity Forum.

1 Source: FIS Real-Time Payments in Asia Pacific

2 FIS Flavours of Fast 2020

3 Applicable in select markets