After a year of unprecedented central bank support, companies with multinational operations are keen to understand the likely path back to ‘normality’. When it comes to central bank policy rates, there is already a clear distinction between the major economies and emerging markets: inflation, and central banks’ credibility when it comes to managing it, will be the key variable.

Figure 1 — Market Data

Once the severity of the COVID-19 pandemic became apparent, most countries adopted a similar playbook of fiscal support and sharply lower official interest rates. In many cases, official rates were cut to record low levels and often below prevailing inflation rates. But the situation has now changed. While the pandemic continues to ravage countries, the focus recently has been on lifting containment measures, spurring economic recovery and creating the conditions for a ‘return to normality’, accepting that the ‘new normal’ may be quite different from the old. So, what happens to interest rates in this environment?

Figure 2 — A Stylized View of Inflation

The key driver is inflation. Most countries experienced lower inflation last year; this year, inflation is generally higher and has increased sharply in a number of countries. How are central banks responding? Virtually all central banks expect that interest rates will increase as part of the return to normal; the issue is the timing and pace of increase.

Major Economies: Delay

Most central banks appear to regard inflation pressures this year as being temporary, arising from supply side problems rather than a resurgence in demand pressures. As such, there is the presumption that interest rate increases are not appropriate. This is the position of the U.S. Federal Reserve, which continues to forecast no change in interest rates until 2023[1] , though recent comments suggest that a scaling back of its quantitative easing program could happen before yearend. In effect, the Fed is basing its interest rate policy on the view that it should raise interest rates to normal levels once the economy has returned to normal. Other major central banks are adopting a similar approach – both in terms of interest rates and quantitative easing. Perhaps the key point is that the central banks of the main industrialized countries have credibility. Financial markets have accepted the view that the spike is abnormal and that inflation will return to normal levels over the next two years, while exhibiting differing views as to the precise timing of any changes.

Emerging Markets: A More Aggressive Response

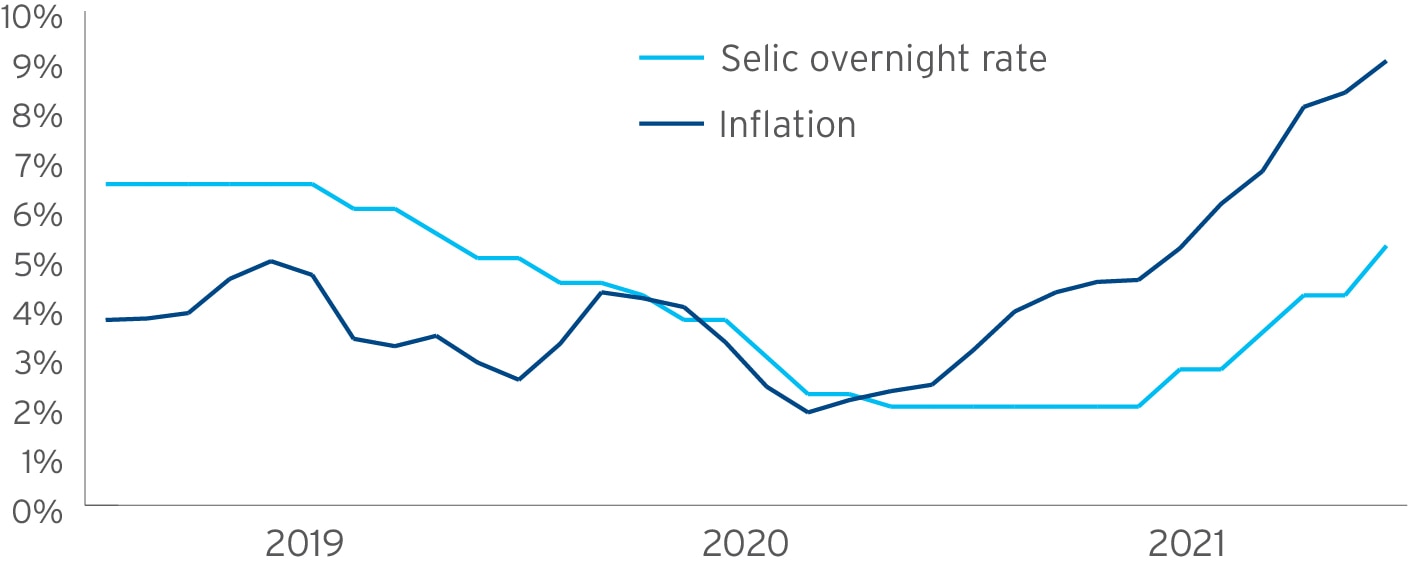

The situation in emerging markets appears quite different. Most notably, the inflation propagation mechanism differs from developed economies. Many central banks face the same supply side inflation problems as their major developed economy counterparts but they do not have the same policy credibility. They cannot allow inflation to pick up without responding because of the risk that it becomes entrenched. Perhaps the best example is Brazil, where inflation has increased from a multi-decade low of just 1.88%[2] in May 2020 to a five-year high of 8.99% in July 2021. When the central bank started raising its benchmark rate (referred to as the Selic) in March — from 2.00% to 2.75% — its goal was to keep the rate below its ‘neutral’ level.[3] But, as inflation continued to increase, it shifted first to a neutral terminal rate and then, most recently, to a terminal rate above neutral.[4] Interest rates have already increased by 325 bps this year and the process is far from complete.

Russia is less extreme than Brazil, but the central bank has raised its benchmark rate by 225 bps to 6.50% since March in response to stronger inflationary increases.[5] The central banks of Latin American countries, such as Chile, Mexico, Peru and Uruguay, have increased rates (Mexico has done so twice) while Colombia is reported to be considering rate increases. In Central Europe, both the Czech Republic and Hungary are raising rates aggressively, while Poland has resisted any change despite inflation at a ten-year high of 5%, well above the 1.5%–3.5% target range. Inflationary pressures have been weaker in Asia, with customers less tolerant of price increases, but South Korea’s central bank is now reported to be considering a rate hike, which would be its first since November 2018.

Figure 3 — Brazil: Inflation vs. Interest Rates

Data source: Bloomberg

[1] https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20210616.pdf

[2] Inflation levels, expressed in %, are change in consumer prices from the previous 12-month period

[3] The neutral level is the level of interest rates consistent with meeting an inflation target over the medium-term.

[4] https://www.bcb.gov.br/en/pressdetail/2407/nota

[5] https://www.cbr.ru/eng/press/event/?id=11077