Selling Globally Across Digital Channels

These days, a digital business like a video game publisher or software company can take advantage of a multitude of digital channels such as app stores, social media, or online marketplaces to quickly extend its reach to a global customer base. In addition to providing a digital storefront, the platforms that provide these channels also facilitate other key functions, such as processing payments from online consumers or invoicing and collecting revenue from enterprise users. Selling online via platforms is the fastest way for digital companies to expand sales and grow revenues.

With the number of digital companies selling globally via digital platforms only expected to increase, it is important for these businesses to be mindful of the implications of their global expansion. When their proportion of foreign revenue grows, so does their risk, and in different ways from traditional companies.

Currency Risk for a Traditional Company vs. a Digital Company

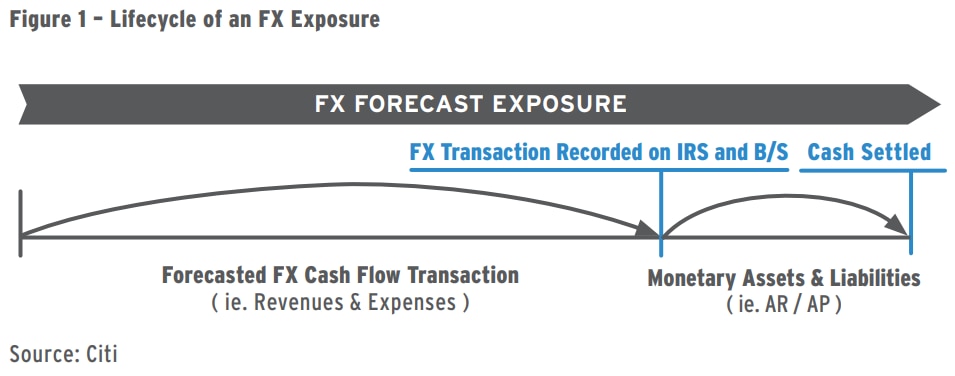

For traditional companies that conduct a significant amount of business in foreign currencies, the leading practice is to strategically manage risk by forecasting currency exposures and establishing FX budget rates. Economically, an exposure starts as a forecast and is managed to protect budget rate. In terms of accounting, transactions are eventually recognized as balance sheet items that are hedged until cash settlement. You can see a typical lifecycle in Figure 1.

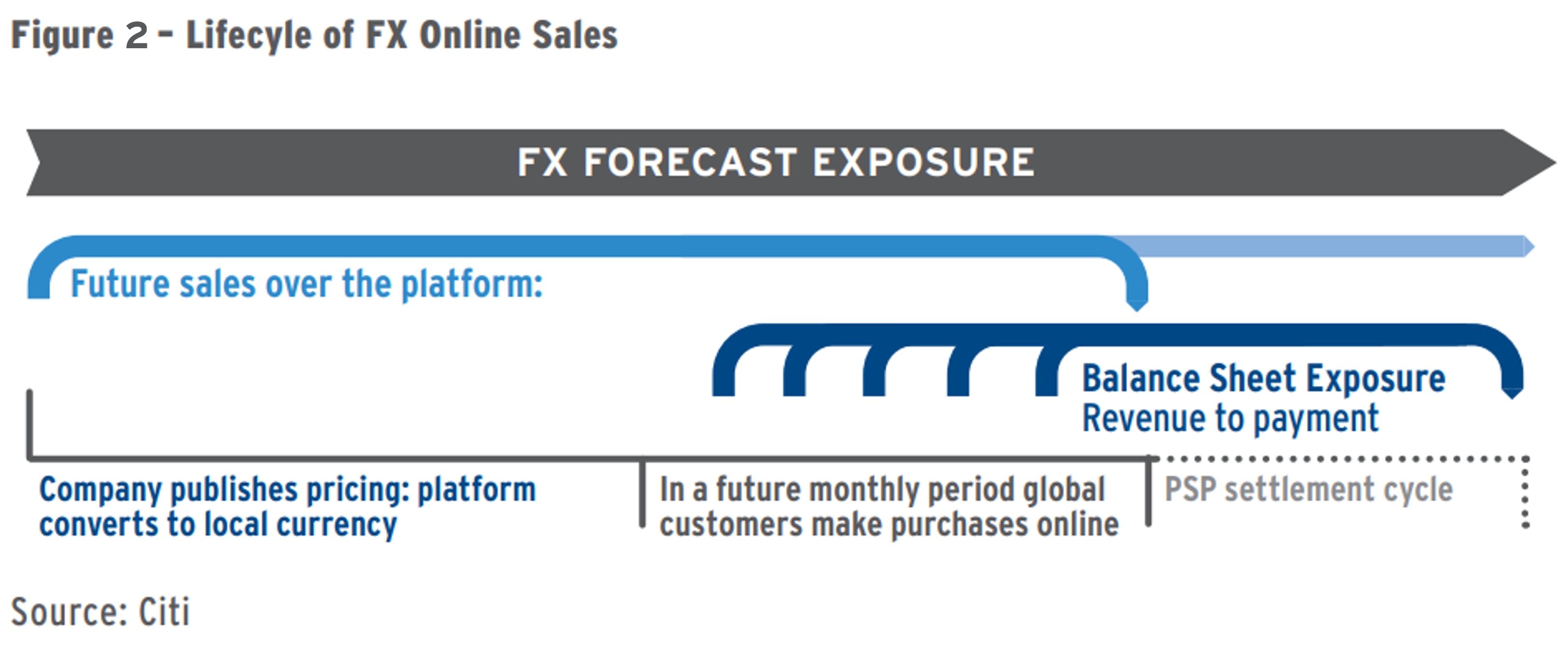

Digital companies operate in a slightly different way compared to traditional companies as their cross-border sales are being enabled by the platforms they work with. Instead of facing FX exposure directly, currency risk is facilitated in the selling process. That facilitation may make it harder to discern the market impact or, worse, give the false impression that there is no exposure. To untangle the impact, we can look at the risk in two phases, shown in Figure 2.

Pricing to Sales

In lieu of pricing in local currencies, digital companies generally view and price their products internally in their chosen functional currency – often in U.S dollar. At a certain frequency, pricing in the functional currency is published and goes live over the digital channel, say an online marketplace. To provide a better local customer experience, platforms offer the option to show those prices in local currency terms at prevailing spot rates. That translation from the functional currency to local currencies establishes implicit FX budget rates.

In an ideal world, if a digital company could publish prices daily and simply pass on the daily FX rate change, there would be minimal FX risk. At 130 USDJPY spot rate, a $100 product costs ¥13,000. If USDJPY moved to 135, the same product would now be listed at ¥13,500. However, frequent price changes could negatively impact purchasing decisions for the consumers. To be able to keep prices constant over a certain period and to give customers a more acceptable experience, companies build tolerance into margin. The same product could still be listed at ¥13,000, but at the current rate in our example, the company earns just $96.30. All businesses face this exposure associated with future sales as markets move, but the unique challenge for digital companies is that exposure is inherently built into the price publication process.

Sales to Payment

After sales occur, the platform usually works with payment processers to collect local currency revenues on behalf of the digital company. If it’s B2B, the platform could also issue invoices and collect revenues that way. In most cases, the platform does this in a batch, collecting sales over a defined period (typically monthly) in local currencies and doing the FX conversions (independently or with payment processors) to send a gross payment to the company in the functional currency. By receiving the functional currencies, digital companies may feel they face no FX risk in the process. Unfortunately, this overlooks the fact that the total payment received depends on FX conversion rates a second time, at a rate that is likely to be different from the rate used when the prices were first published over the platform.

From an accounting perspective, when sales occur, revenue is recognized (likely at a daily rate). If the platform/payment processer converts FX sales daily, then the receivable would be immediately relieved into the functional currency. But as we saw earlier, it is more likely that the platform is converting sales only once a month, which means that an FX receivable could sit on the company’s balance sheet for 30 days, and changes in the amount eventually received would impact earnings.

A Word About FX Risk Management

The scenarios above make life more difficult for a digital company that is trying to streamline its operations and avoid surprises stemming from exposure risk. To manage this, hedging programs can be constructed to cover the two phases of risk:

- Pricing to sale: When the local pricing goes live, hedges can be executed at the time of price publication to capture the spot rate and protect sales at that rate. To do this would require a forecast of total sales. As companies mature and gain sales data over time, this may become more viable.

- Sale to payment: A derivative hedge can be executed to offset risk between when daily sales/revenues are recognized and when the platform ultimately converts cash from customers to the functional currency. Because sales can involve multiple transactions, this is an area where innovation from banks on automated solutions may be beneficial. Digital companies can potentially leverage automation to achieve efficient execution and booking of hedges.

In Conclusion

Online platforms can have the major benefit of quickly bringing a digital company’s products to the world. But companies selling on these platforms should be aware of where currency exposures arise and how they face different challenges from traditional companies. If they understand that exposures begin from the moment of price listing and continue through to when foreign sales are collected, converted and received, they can begin to take steps to mitigate their risks and streamline their cash flows.